Gabriel Collins

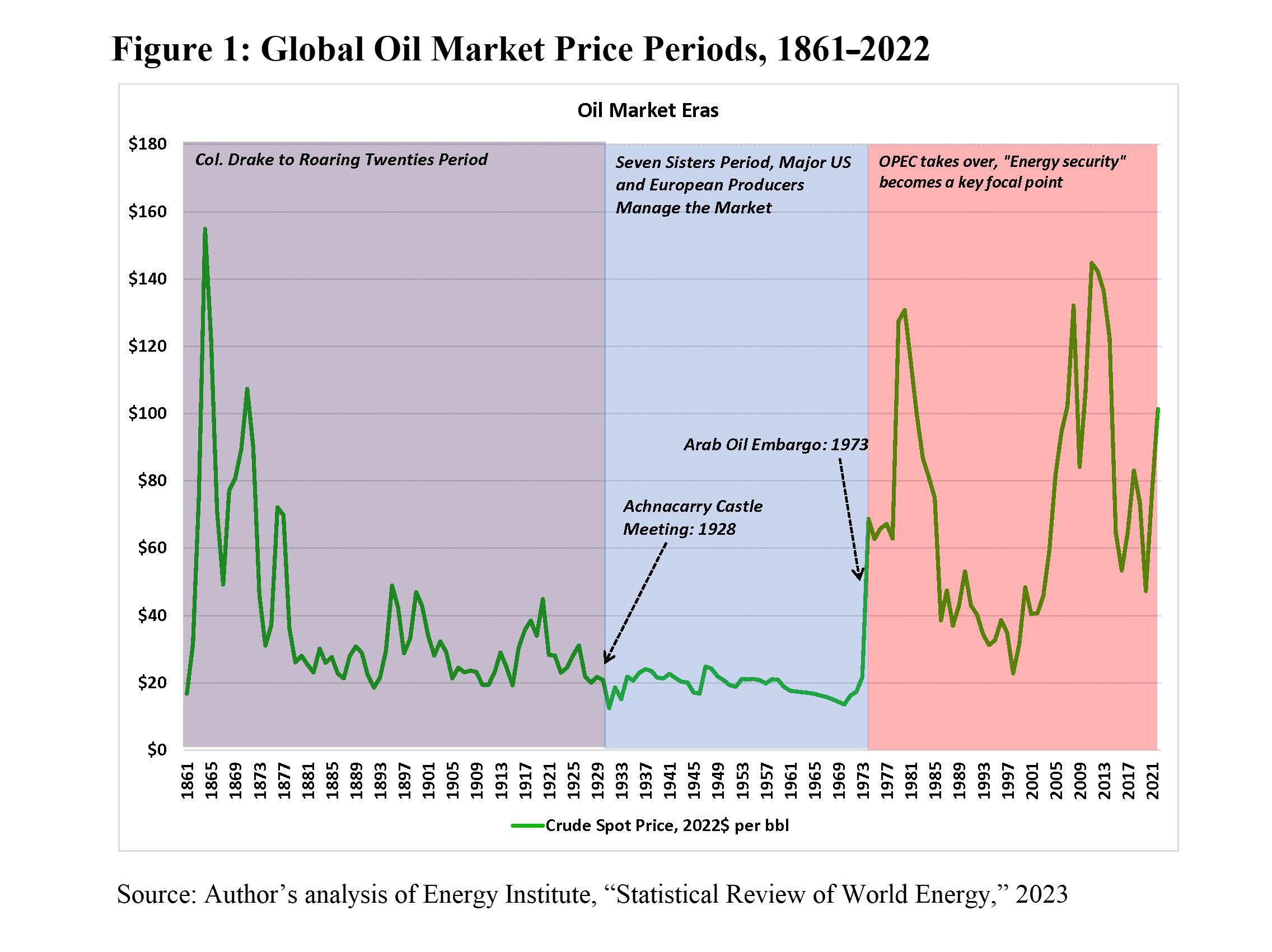

“Energy security” is broadly defined in the literature as meaning the reliable and affordable supply of energy, but discussions are often decidedly oil-centric. Indeed, both academic and policymaker attention to energy security as contemporarily defined only began to rise after market turbulence in the late 1960s and then the 1973 oil embargo ended a nearly 50-year period in which a handful of major U.S. and European international oil companies effectively controlled global prices (see Figure 1).1 As a simple barometer, a search for journal articles containing the term “energy security” on JSTOR yields 5,590 results, but only a few dozen predate 1973. Oil’s pervasiveness in modern economies and its status as the world’s most widely traded commodity explain why “energy security” is often equated with “oil security.” After all, an attack on a single facility in Saudi Arabia can within minutes trigger a 15% spike in oil prices worldwide—and prices of fuel are one of the few topics of broad, global common interest in today’s polarized world.2

{kind=link}

The disproportionate prominence of oil obscures in plain sight the vast energy ecosystem underpinning the modern world. This essay departs from existing literature by pinpointing and analyzing a much deeper and different strain of thought among officials from the People’s Republic of China (PRC), one that recognizes oil’s importance but which permits a more holistic analysis. Other authors have hinted at these interconnected energy realities at the global level.3 Yet to this author’s best awareness, none have engaged primary documents—and perhaps more importantly, “primary data”—to empirically assess how the PRC officials and firms shaping the world’s largest energy system think about energy as a strategic space in which to manage risk and secure competitive advantage. Specifically, this essay analyzes hard data reflecting consumption, production, and investments in the energy space by PRC entities.

Energy’s Unique Character Drives Unique PRC Security Responses

Energy involves both the physical world of heat, flame, splitting atoms, and spinning turbines as well as the more ethereal—but incredibly powerful—world of globalized markets. It also presents unique analytical opportunities. Strategists studying war and long-term strategic competition rarely receive real-time feedback from the world around them (apart from wars like those underway in Ukraine or Israel). Episodic events force a heavy reliance on backcasting and parsing the past for clues about the present. Hence, the use of the time-worn adage that “generals always fight the last war.”

Energy is very different because energy “war” is being fought constantly in real time as companies, consumers, and countries iteratively prepare for the “next” campaign. Energy activities are also harder to hide than military ones due to their sheer scale and distinct signatures. Even when Beijing seeks to conceal activities, they often reveal themselves through flows of physical goods, capital investments, and various emissions such as heat, methane, carbon dioxide, oil tank roofs, coal piles, dams, nuclear reactors, wind turbine and solar farms, and land-use changes that can be tracked by satellite. Words matter but actions speak far louder.

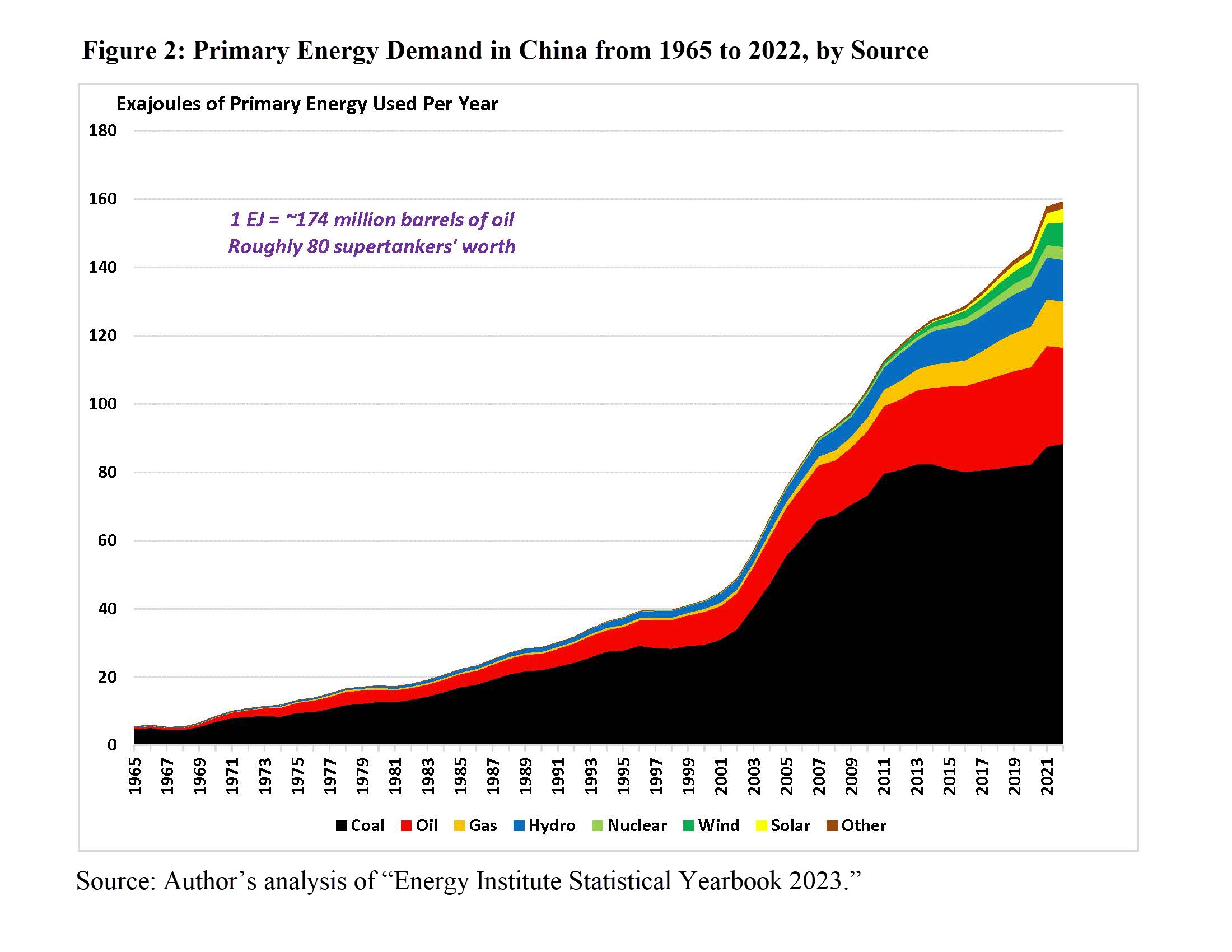

Energy security is national security. Energy drives economic competitiveness (and by extension, national power) and, at the most basic level, underpins modern civilization. We need it to cool off and stay warm, access clean water, remove and treat sewage, or bring essential foods and other items from producers to consumers. This is especially true for China, where basic, energy-intensive industries remain systemically important economic engines and the national energy system is now about 1.6 times the size of that of the United States, the planet’s second-largest consumer (see Figure 2).

{kind=link}

Scholarly writings and lived action also suggest that Chinese policymakers think differently about energy and its role in a nation’s competitive position and well-being than do many of their counterparts in the Organisation for Economic Co-operation and Development (OECD) world. The International Energy Agency—a proxy for liberal, global market-based approaches—defines energy security as “the uninterrupted availability of energy sources at an affordable price.”4 Member countries (including the United States) have worked to create a coordinated system for managing strategic oil reserves, share information through fantastic data resources like the Energy Information Administration (EIA), and generally leverage transparency and market forces to achieve their objectives.

PRC energy policymakers tend to take a different approach. They harbor a quasi-autarchic mindset rooted in decades of policy premised on fearing and avoiding interdependence and imports. Stripping complex equations and regression analysis from contemporary PRC scholarship on energy security frequently leaves behind a stark conclusion: the more energy a country can source from within its own borders, the better off it will be.5 General Secretary Xi Jinping’s admonition to delegates of the 20th Party Congress in October 2022 that China must “be prepared for the worst-case scenarios, and be ready to withstand high winds, choppy waters and even dangerous storms” exemplifies this worldview.6 Xi has made clear that energy is part of this stormbreaker strategy, telling workers at China’s second-largest oilfield in October 2021 that the country must “ensure that its ‘energy rice bowl’ remains in its own hands.”7

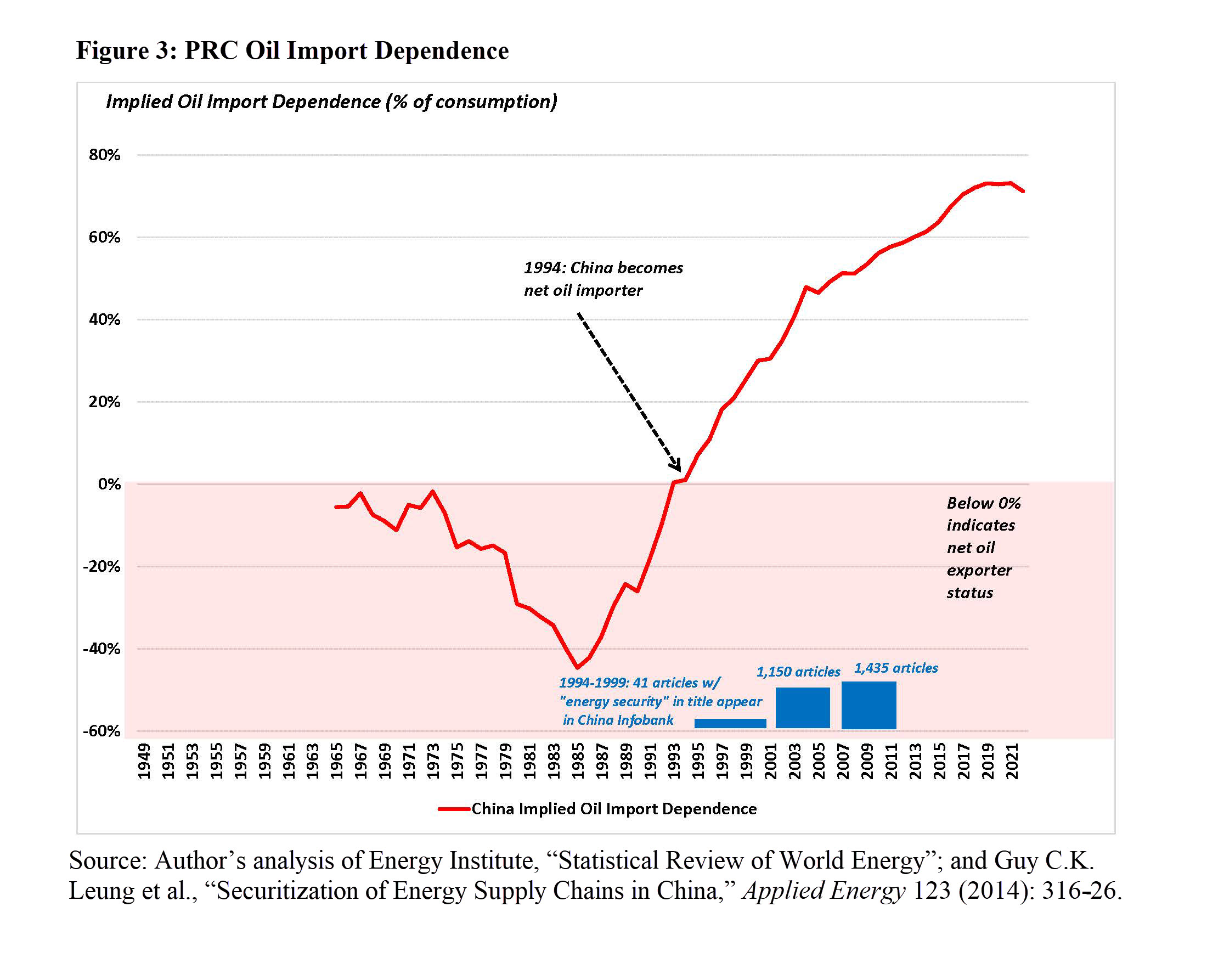

Previous oil trade embargoes by the Soviet Union and the United States during the Cold War have reinforced the self-reliance (zili gensheng) mindset. Energy-oriented sanctions and economic warfare measures by the OECD countries over the past 25 years likely have further amplified concerns, especially as the advent of U.S. domestic oil abundance and rising PRC oil import dependence coincides with a period of sharper economic coercion by each party, including export controls on rare earths, semiconductors, and other goods (see Figure 3).

{kind=link}

China’s broader anxieties about energy security center on oil in part because the country lacks domestic resources, cannot create new ones through application of its industrial prowess, cannot control events abroad in producing regions, and is vulnerable to naval blockades.8 Interviews conducted around a decade ago highlight the different views of oil relative to other energy sources. PRC energy technocrats noted that electricity supply “problems can be solved by ourselves,” but that “oil imports are different”: “If our oil imports are cut off, it affects the whole nation, not just certain provinces, and we no longer maintain zili gensheng [self-reliance].”9 Reliance on oil imports appears to be especially jarring for a PRC leadership that seems to have concluded that the world is heading into a potentially prolonged period of chaos.10

China is in a much more sensitive energy position in what some are terming the “second cold war” than the Soviet Union, invulnerable due to oil and gas self-sufficiency, was in the first. Moreover, by adopting a more militarized forward oil supply defense posture, such as deploying forces capable of high-intensity naval combat against nation-state foes and the necessary supporting infrastructure, the PRC would risk diluting the combat power available in its highest-priority operational theaters: the Taiwan Strait, East China Sea, and South China Sea.11

The PRC Tries to Build Its Way to Energy Security

Beijing’s response to date instead has emphasized maintaining larger oil inventories, managing fuel demand through price, and seeking to become an “electrostate” that substitutes electrons for oil.12 Electrostate policies also include moving to secure globally influential positions on both higher-value-added industrial chains for alternative energy goods like batteries and electric vehicles (EVs) while also exerting deep, intentional influence over physical supplies of energy raw materials. The PRC also seeks commanding positions astride global energy data flows that can give its parastatal firms competitive advantages and improve strategic visibility into ally and adversary economies alike.13

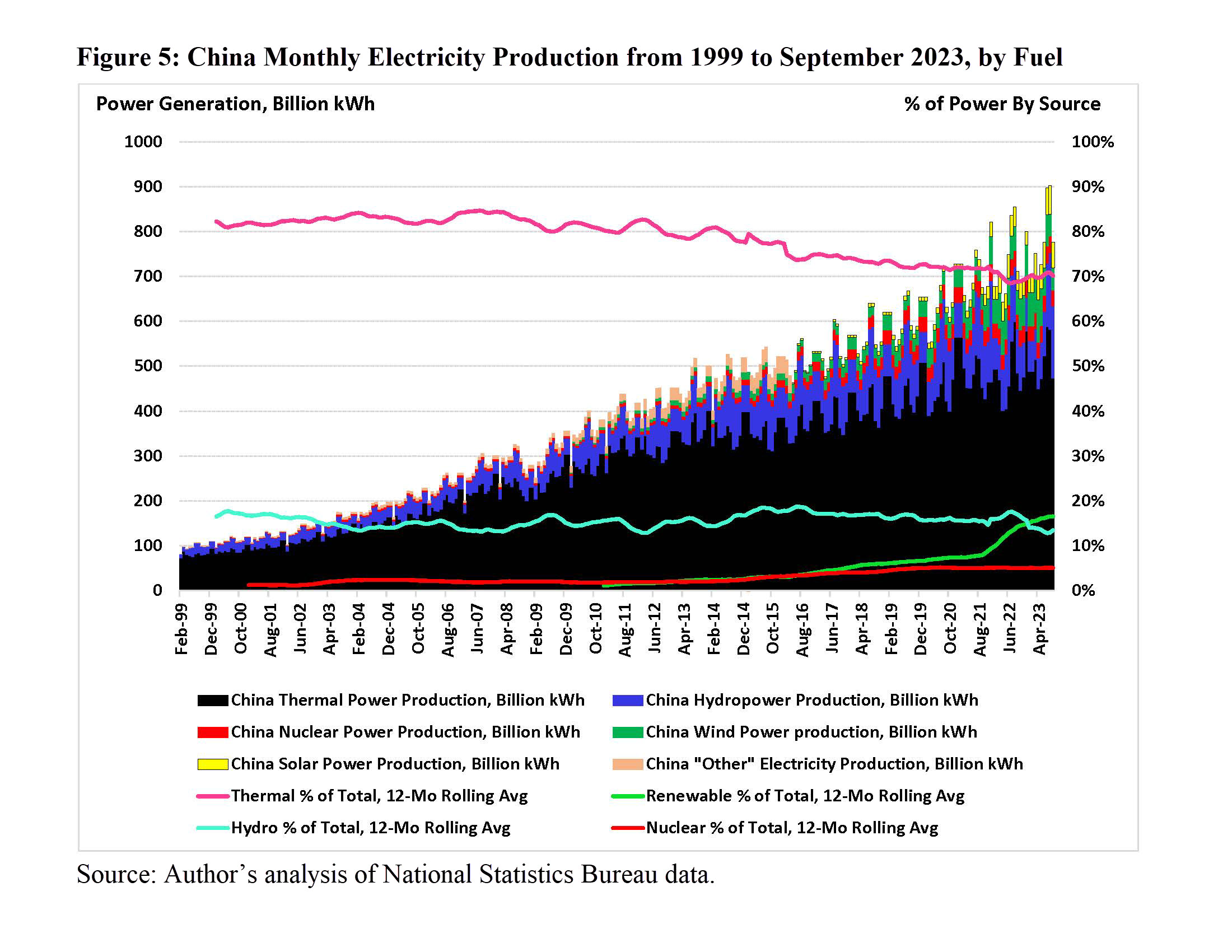

Building an electrostate requires several core elements. First, there must be a steady baseload supply because the more electrified an energy system is, the worse the economic and political impacts of power shortages will be. In China’s case, this means that coal remains the literal bedrock of the energy system, with thermal power (primarily from coal) still providing about 70% of national electricity supply and a major portion of industrial process heat (see Figure 4). Even if coal’s share of total energy use is gradually declining, absolute usage has risen and is likely to remain robust for many years. Indeed, the PRC National Energy Administration published a position statement in April 2022 on energy security that reiterated coal’s role as a foundational resource for China and emphasized the importance of maximizing self-sufficiency in this resource (see Figure 5).14

{kind=link}

{kind=link}

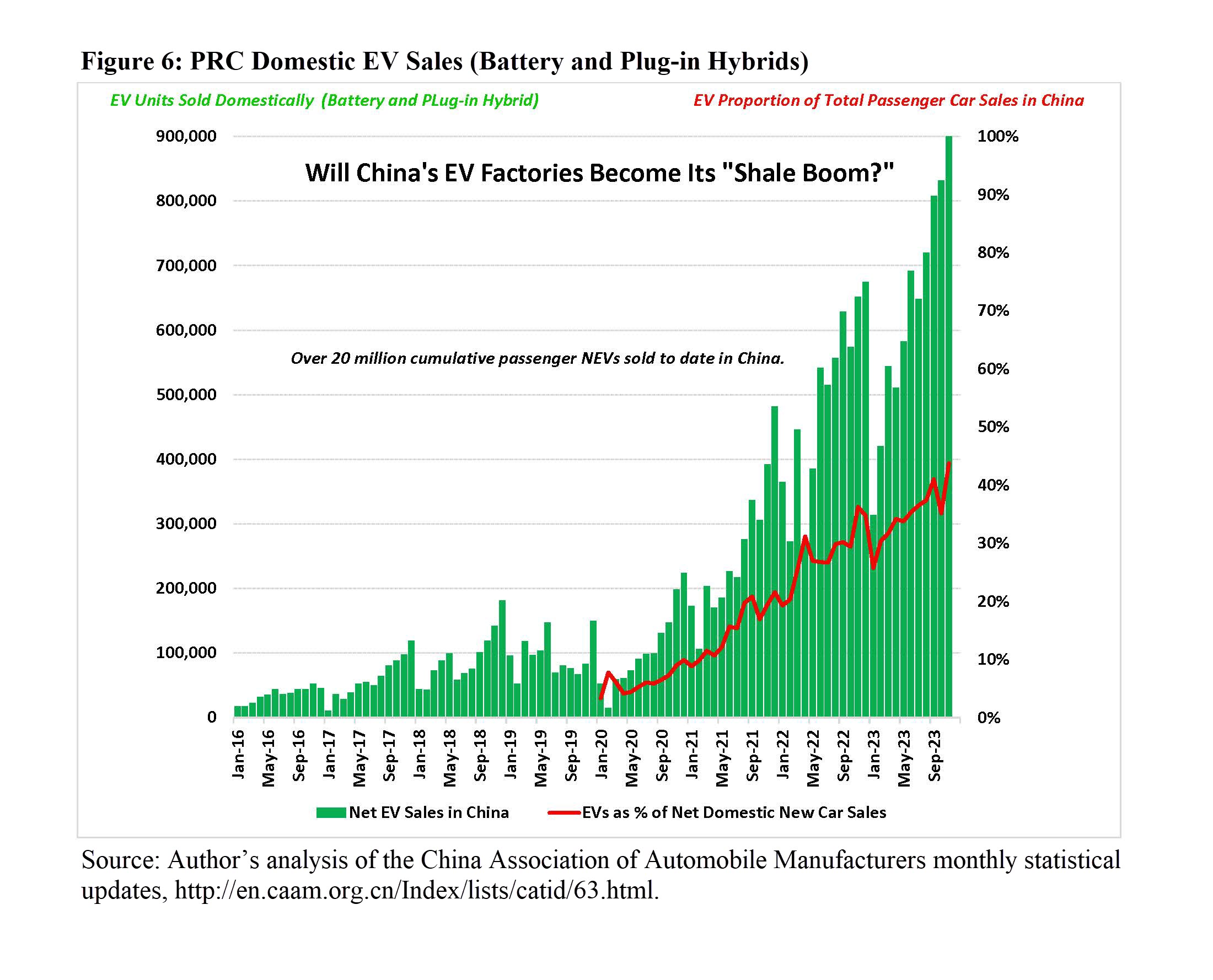

Second, transportation electrification and the associated value chains are the product of decades of efforts that, after what are likely hundreds of billions of dollars in collective investments, are now finally able to scale. EVs began to receive much more policy attention in China during the early 2000s, including from the 863 Program (State High-Tech Development Plan), presaging their role in the Made in China 2025 plan roughly a decade later. Official focus intensified with the 2007 appointment of Wan Gang as minister of science and technology.15 A German-trained former Audi executive, Wan was appointed by then premier Wen Jiabao and attracted strong support from China’s national security community, which perceived the country’s rapidly rising oil imports as a strategic vulnerability. Bracketed by security actors concerned about oil import dependence and techno-industrialists seeking new economic advantages, China’s EV sector has blossomed. Battery EVs and plug-in hybrids accounted for one-third of new vehicle sales in China through November 2023, with more than 20 million passenger EVs cumulatively sold (see Figure 6).

{kind=link}

Third, as the share of intermittent renewables in total power generation increases, Chinese grid operators will need to maintain stability through expanded storage as well as ensuring that sufficient dispatchable power capacity exists (i.e., coal, gas, or nuclear) to balance the system. During extreme weather events in the United States, EIA data shows that on a week-to-week basis, gas inventory withdrawals can rise as high as 50 billion cubic feet per day (equal to half of preexisting daily demand) to balance the system as consumers scramble to heat, cool, and generate electricity.16

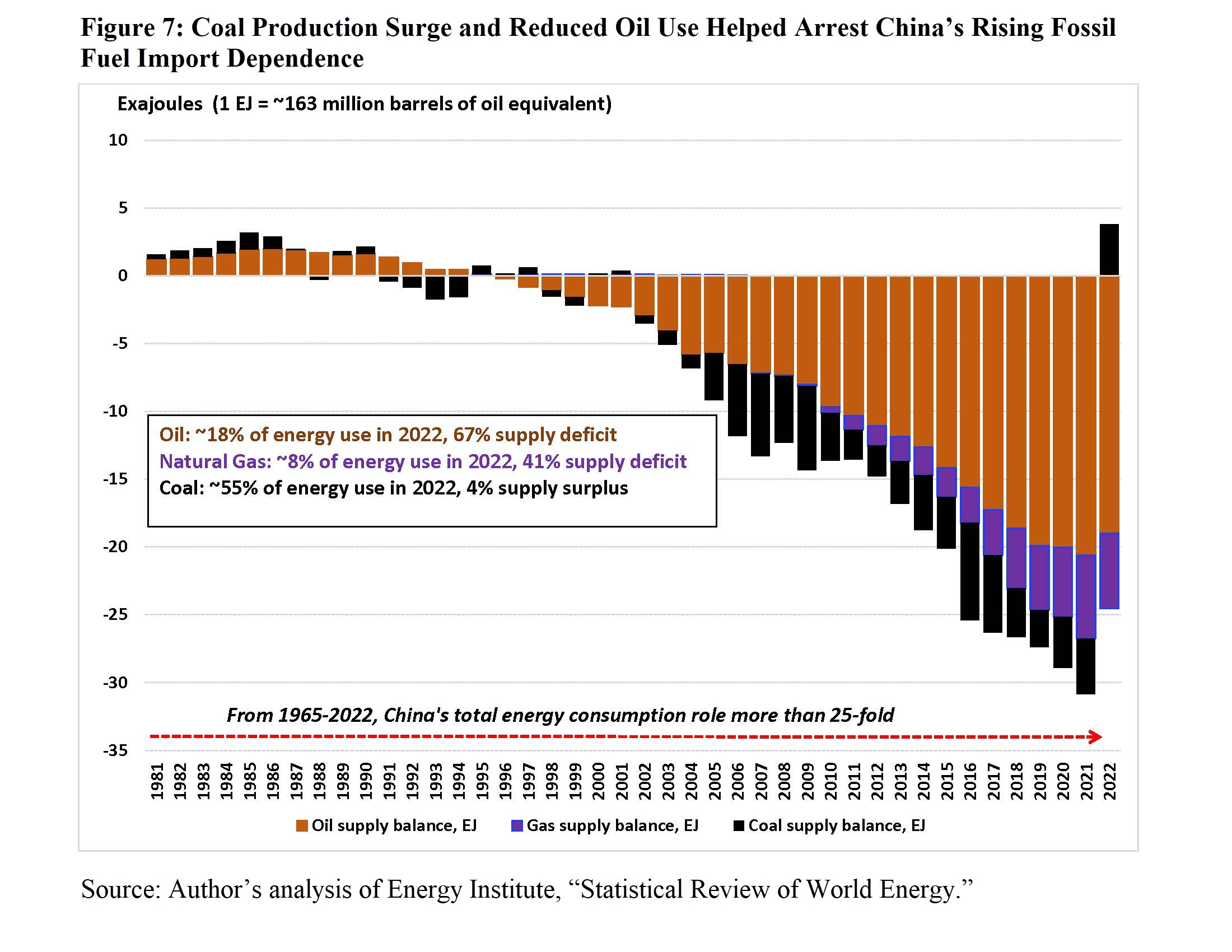

Adjusting for the larger size of the Chinese energy system and its use of coal as the foundational fuel rather than gas, similar weather-driven events could conceivably trigger incremental energy use equal to more than 8 million tonnes per day of coal—a significant portion of underlying daily average demand. Coal is the only energy resource in China that is currently capable of surging on short notice to meet such demand. Figure 7 shows the net impact of coal production that rose sharply in China during 2021 and 2022 as Chinese authorities grappled with blackouts. Beijing likely realized that only two energy sources could be rapidly procured to fill supply gaps—imported oil, as was done in 2004, or domestic coal. The latter is a fuel more congruent with PRC national security concerns and can be rapidly plugged into a terawatt-scale coal-fired power plant base that was underutilized in many areas.

{kind=link}

The Newest Energy Battlefield: Data

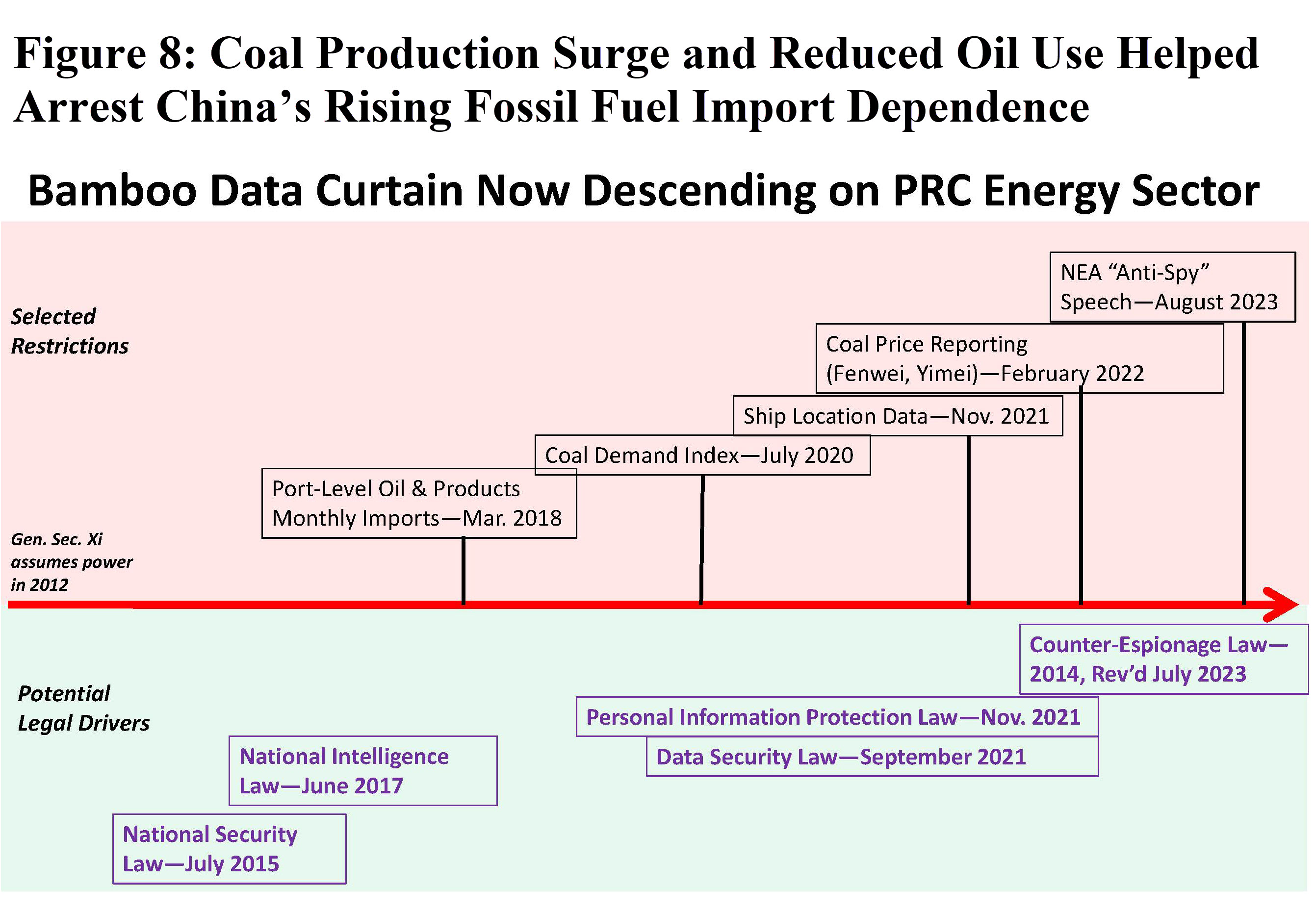

Chinese leaders’ evolving conception of energy as a strategic space also demands that they control as much of the associated data as possible. Over the past five years, China has progressively curtailed key streams of energy-related data available to the outside world. Port-level oil and refined products import data was among the first sources to face restrictions, followed by sources for coal demand, ship locations, coal pricing, and now even basic weather data (which is foundational for energy demand analysis).17 In the author’s experience, since the onset of the Covid-19 pandemic in 2020, other important energy data such as provincial-level daily electricity information that used to be published regularly is now only available intermittently and in partial form (see Figure 8).

{kind=link}

This descending “bamboo curtain” will make analysis harder, muddle important investment and trade flow signals, and increase the importance of remote sensing. PRC authorities may also abuse data asymmetries to try and privilege China-domiciled firms, shape market activities in the PRC’s favor, and deepen the country’s informational advantage by continuing to collect data from abroad and fusing it with local data flows that are now effectively proprietary under pain of legal prosecution.

PRC entities could increasingly leverage this energy data asymmetry (including the injection of strategic insider knowledge from the highest levels of government) to facilitate trading operations by parastatal firms that lock in profits and strategic positions to the detriment of the United States and key U.S. allies. For instance, PRC entities bought more than 90% of all global long-term liquefied natural gas contracts in the six months leading up to Russia’s invasion of Ukraine, soaking up gas now badly needed by consumers in Europe, even though China’s own gas demand was and is stagnating and domestic coal production was surging and remains historically high.18 State-aided trading activities can amplify this competitive advantage, given that countries exposed to energy price volatility incur massive costs that drag down industrial activity and court political disruptions by consumers facing “heat or eat” decisions. Russia’s war on Ukraine, for instance, has cost Europe around one trillion dollars to date.19

Conclusion

PRC leaders’ statements and actions reveal energy to be a critical strategic space. They also reveal an understanding of energy security that seeks to move beyond oil centricity to a more holistic approach. Oil is treated as part of a larger energy and resilience policy package, and notably the bits and bytes of energy-related data flows are placed on a similar strategic plane as the molecules themselves. To that point, China’s evolving approach to energy flows and the data associated with them also strongly suggests that energy will not be a cooperative space (as it often is between OECD countries), but instead an intensely competitive one.

Competition will play out on the techno-industrial plane, as well as the geopolitical and informational levels. In Chinese foreign policy, climate change does not hold the same environmental and moral importance that it does for many U.S. policymakers. Beijing’s fundamental goal remains promoting the Chinese Communist Party’s rule, image, and influence. It can further this goal through participating in the global green economy by selling EVs and batteries, rare earth minerals, and wind turbine components. Or it can use climate negotiations to demand that the United States and others accommodate Chinese economic, political, and security imperatives in exchange for promises that will likely remain unfulfilled. This will likely include climate influence operations that seek to harness domestic constituencies to build virtual gates and walls that more broadly constrain the United States’ freedom of action in the Indo-Pacific and countermeasures to pernicious PRC behavior.20

In the ongoing multi-decade competition between China and the United States for regional and global preeminence, energy will be a foundational strategic space. Energy and techno-industrial competition between the two powers that account for around 40% of global energy use and emissions will shape the world for years to come.

No comments:

Post a Comment