CARLA NORRLÖF

America’s pandemic policies and the broader response to Russia’s war on Ukraine have unleashed widespread speculation about the future of the US dollar’s global hegemony. Yet one should not assume that a more divided world will automatically give way to a more multipolar one, especially where reserve currencies are concerned.

America’s pandemic policies and the broader response to Russia’s war on Ukraine have unleashed widespread speculation about the future of the US dollar’s global hegemony. Yet one should not assume that a more divided world will automatically give way to a more multipolar one, especially where reserve currencies are concerned.TORONTO – In this new era of geopolitical upheaval, business leaders, politicians, policymakers, and academics are anticipating a more fragmented, multipolar world order, with many predicting especially consequential changes in the international monetary system. America’s pandemic policies and the broader response to Russia’s war on Ukraine have triggered widespread speculation about the future of the US dollar’s hegemony, and while warnings about the eclipse of the greenback are not new, some commentators believe that this time is different.

True, high inflation, rising US public debt, and other key developments are unfolding in a strategic environment that is increasingly reminiscent of the Cold War. The most striking parallel is the return of great-power rivalries and policymakers’ preoccupation with security concerns, which are taking precedence over economic efficiency. But while the elevation of security issues is clearly reshuffling some alliances and economic relationships, it is unlikely that these changes will usher in a multipolar currency system in the foreseeable future.

The biggest problem with the narrative about fragmentation and an inexorable drift toward multipolarity is its imprecision. The term “multipolarity” is rarely defined; and even when it is, it is used inaccurately. Moreover, one should not assume that a more divided world will automatically give way to a more multipolar one, especially where reserve currencies are concerned.

SHOCKS TO THE SYSTEM

The past three years have certainly tested economic interdependence. Inflationary food and energy insecurity collided with the US Federal Reserve’s response to the pandemic, which included extending dollar swap lines to other central banks and lowering interest rates through bond purchases and other measures. These policies increased the supply of dollars worldwide at a time when supply-chain disruptions were hampering trade and driving down stock markets.

Worse, even before the recent shocks, geopolitical tensions were rising amid spats over trade and investment, as well as over the uses of economic coercion. While relying on economic measures to achieve foreign-policy goals is preferable to military means, it also risks infusing economic relations with conflict. In this new geopolitical game, the United States, China, and Russia each play to their strengths, using the levers of finance, commerce, and energy to create opportunities for themselves and strike at other countries’ weak spots.

ISABELLA M. WEBER urges policymakers to match their improved understanding of the problem with more appropriate policies.

This trend lends credence to fears about economic decoupling, deglobalization, and fragmentation. On the monetary front, the worry is that countries anticipating US sanctions will move pre-emptively to reduce their dependence on the dollar. China and Russia have been especially energetic in pushing alternative currencies and building a multinational financial infrastructure for trade and investment in renminbi and rubles. For example, China’s Cross-Border Interbank Payment System (CIPS) acts as a clearing house and is thus similar to the US Clearing House Interbank Payments System (CHIPS).

Of course, CIPS processes a mere 15,000 transactions per day, amounting to the dollar equivalent of $50 billion, whereas CHIPS processes 250,000 transactions per day, with a value exceeding $1.5 trillion. But it nonetheless has laid the groundwork to clear and settle more cross-border exchanges in renminbi. When China launches a financial messaging system capable of working independently from the Society for Worldwide Interbank Financial Telecommunication (SWIFT), it will have its own complete, autonomous architecture for settling cross-border transactions denominated in its own currency.

For its part, Russia has already taken steps to bypass SWIFT, creating its System for Transfer of Financial Messages (SPFS) after its illegal annexation of Crimea in 2014. Russia’s central bank claims that demand for SPFS has increased significantly since last year’s full-scale invasion of Ukraine. By the end of September 2022, however, the system had only around 440 users.

Still, owing to the new payments infrastructure and various bilateral agreements, pursuing trade and investment in non-Western currencies has become somewhat easier. Russia and China have agreed to trade in renminbi; and Russia and India planned to trade in their own currencies following Russia’s full-scale invasion of Ukraine by reviving the Cold War-era rupee-ruble mechanism. The latter effort was recently discontinued, however, with both countries routing trade through the United Arab Emirates instead, taking advantage of the dirham’s dollar peg while avoiding explicitly settling trade in dollars, rupees, and rubles. All told, such use of alternative currencies by third countries remains small. While the renminbi is being used to settle a Russian investment in a nuclear-power plant in Bangladesh, similar other examples are scarce.

Governments are also making plans to move away from pricing oil in dollars, although the significance of this development is easily overstated. Oil may be one of the world’s leading export products, but it ultimately accounts for a very small share of total global trade.

More broadly, because international currencies are, by definition, used by third countries, adopting a trade or investment partner’s currency will not necessarily raise that currency’s international role, even if it does reduce the greenback’s relative role in cases where those transactions were previously denominated in dollars.

GLOBAL YUAN OR TOTAL YAWN?

Those predicting the end of dollar hegemony also point to China’s own use of bilateral swap lines to allow foreign central banks to acquire renminbi in exchange for their own currency. Making renminbi available to foreign governments is a prerequisite for its use by public and private actors, and the ability to act as lender of last resort in times of crisis is a key reserve-currency function.

China has also been maneuvering to expand its institutional footprint, such as by introducing an emergency renminbi liquidity arrangement under the auspices of the Bank for International Settlements (BIS). Similarly, the basket of currencies underpinning the International Monetary Fund’s special drawing rights (SDRs, the IMF’s reserve asset), now includes the renminbi, alongside the dollar, yen, euro, and pound sterling. And the BRICS (Brazil, Russia, India, China, and South Africa) have also discussed ways to push back against dollar hegemony, such as by issuing a joint reserve currency to bypass the dollar and other major Western currencies (as well as offering an alternative to SDR).

Finally, one of the most eagerly anticipated technological developments in this area is China’s creation of digital payment alternatives. China’s central bank began developing a digital currency, the e-CNY, in 2017 and offered this payment option to participants at the 2022 Olympics in Beijing. When fully implemented, the e-CNY will function independently of other payment and financial messaging systems. By offering cheaper, faster, and safer transactions, a Chinese digital currency could make the renminbi more attractive and therefore more widely accessible and liquid. Promoting the e-CNY for trade and investment could accelerate renminbi internationalization.

But underlying trade and investment patterns must change before the global currency hierarchy does. Here, the China-centered Regional Comprehensive Economic Partnership, as well as China’s Belt and Road Initiative, could help internationalize the renminbi by multiplying economic interactions and encouraging renminbi use in third-country trade and investment. Still, in the medium term, renminbi internationalization is likely to encounter substantial hurdles, owing to China’s maintenance of capital controls and broader balance-of-payments constraints.

MULTIPOLARITY FEVER

Despite these obstacles, speculation about a coming multipolar currency order is rife. But what does multipolarity really mean in this case? Some prominentcommentators, such as former Bank of England Governor Mark Carney and Zoltan Pozsar of Credit Suisse, neglect to define the term precisely. Others foresee a system where a few currencies are symmetrically distributed. And still others anticipate a world populated by many major currencies.

Hence, François Villeroy de Galhau, the governor of France’s central bank, believes we are moving toward a beneficial “balanced multipolar system.” European Stability Mechanism Managing Director Klaus Regling echoes this view, anticipating a multipolar currency system “with about equal rates [of usage] for dollar, euro, and renminbi.”

Those who focus more on the number of currencies fulfilling reserve-currency status include Barry Eichengreen, who argued back in 2009 that “the international monetary system will become more multipolar” along these lines. But while Eichengreen presciently predicted the renminbi’s rise as a reserve currency, his implied definition of a multipolar system is problematic, because the existence of multiple reserve currencies throughout the post-war era suggests that today’s international monetary system has always been multipolar.

Identifying reserve currencies is a necessary first step in determining the polarity of the international monetary system, but it is not sufficient, because it does not help us determine whether and when we have crossed the Rubicon into multipolar or bipolar territory.

Polarity is a term traditionally used by international-relations scholars to assess the global, systemic balance of power on the basis of military might. But since the concept travels well, it has also been applied to other areas, such as economic power. In fact, it is particularly well-suited for characterizing the international currency system, because great-power currency capabilities can be used to enforce international agreements and police international order.

In a unipolar currency order, one great power enjoys preponderance and has no close rival. In a bipolar currency order, two powers predominate and have only distant rivals. And in a multipolar currency order, more than two great powers wield relatively equal influence. Yet this still leaves open the question of how to measure polarity.

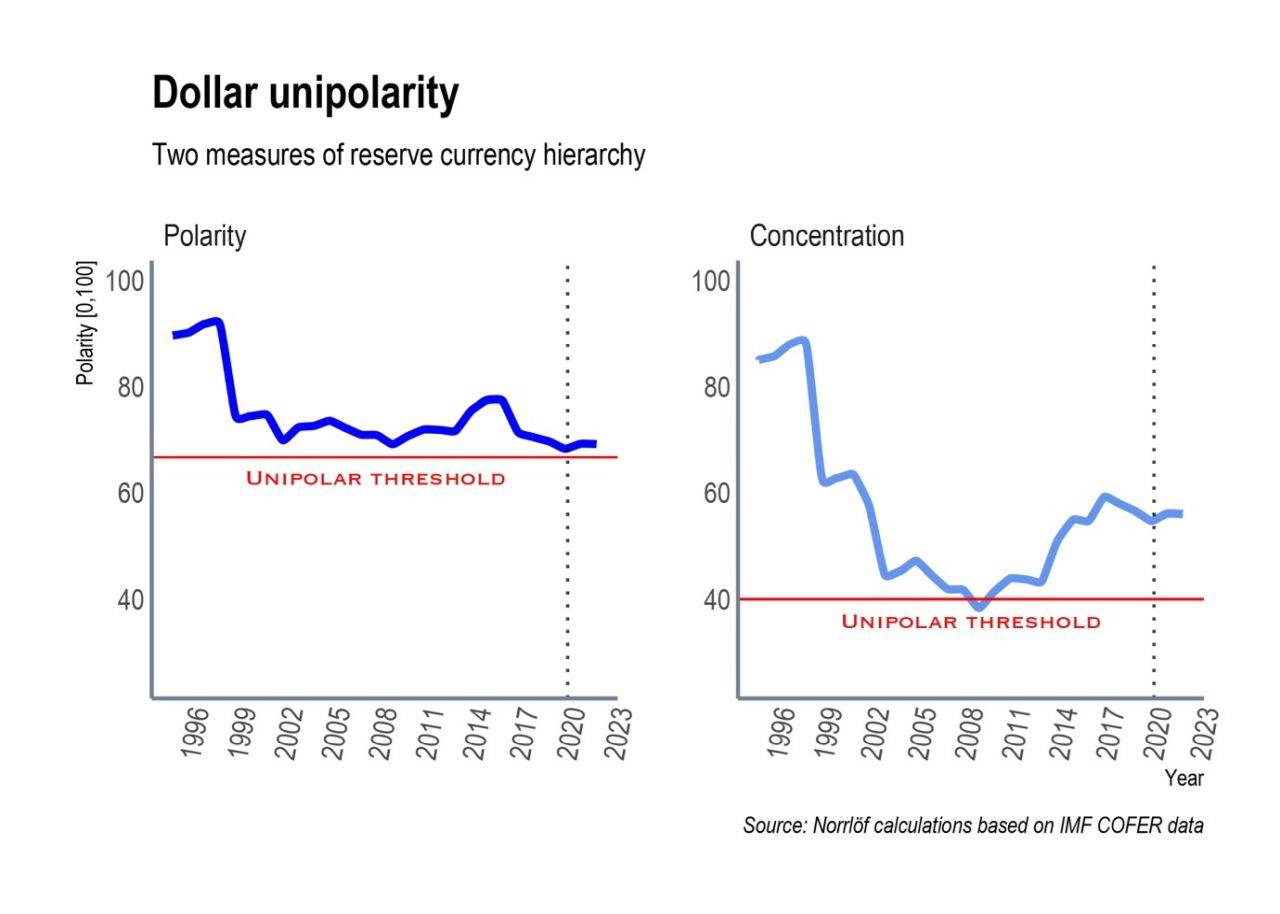

In the accompanying figure, I have measured reserve-currency polarity in two ways to establish a unipolar threshold. The first panel counts the number of great powers according to some predefined yardstick, singling out reserve currencies based on their share of known reserves (with a 5% cutoff). A unipolar line is drawn at a level where reserves in the leading currency are twice as large as reserves in other major currencies. This standard offers a clear-cut abstraction of unipolarity. Being twice as powerful as any counter-coalition clearly renders a balance of power impossible and thus creates stability by muting opposition.

But unipolarity can also prevail without this rather exacting standard, as in the right-hand panel. Here, the unipolar line is based on system-wide changes in currency shares. A unipolar threshold is drawn at a concentration index of 40, below which point the system no longer is considered unipolar, but rather bipolar or multipolar.

There are striking differences between the trend lines in the figure’s two panels, and in terms of unipolar wiggle room. The “great currency” distribution measures the relative influence of reserve currencies capable of playing an international role. Here, the long-term power gap has been closing. In fact, we were skating closer to the unipolar threshold before the pandemic erupted in 2020, and before sanctions were levied against Russia for launching its all-out war against Ukraine.

Now, because the primary currencies comprised in this measure are all part of the Russia sanctions coalition, attributing changes in this distribution to sanctions backlash is a stretch. That brings us to the second panel, which portrays systemic concentration, a measure of the relative influence of all currency reserves within the system. Here, the long-term distribution of power remains largely unchanged – though a post-pandemic, post-Russia-sanctions decline is discernible.

If we base our predictions about the longevity of the unipolar currency era on the first panel, the situation looks rather dramatic. Even so, a dip below the unipolar threshold would bring us to the world envisaged by Kroll Chief Economist Megan Greene: “In a multipolar world, we may eventually be talking about alternatives to the dollar. But we won’t be replacing it.” From the vantage point of the second panel, however, unipolarity is as entrenched as it was before the euro launched.

DOLLAR DOMINANCE

How we measure polarity matters enormously for debates about the future of the international monetary system. While polarity, understood as the distance between the “great currencies,” has declined over time, it has not done so since 2020. By contrast, polarity, understood as system-wide currency distance, has been constant since 1995 but did decline from 2020.

Economists’ reluctance to define multipolarity has fueled a mania that is unhelpful for adjudicating major US foreign-policy decisions. We are inundated by predictions of a shift to multipolarity without knowing what it means, and when, in reality, the eclipse of unipolarity would more likely be followed by a bipolar order fixed around the dollar and the euro.

Moreover, it is unlikely that unipolarity will fade at all any time soon – or even in the medium term. That will remain the case even in a more fragmented global economy where security partnerships determine economic relations, and where sanctions against Russia contribute to a realignment of some global currency holdings. The pandemic and recent geopolitical developments do not justify confident bets on the dollar’s demise, because the greenback’s centrality is mainly determined by economic factors and an incumbency advantage that is reinforced by network effects.

Remember, today’s inflation is not just a US phenomenon, and when considering sanctions risk, diversification out of dollars must be weighed against sanctions-induced diversification into dollars. The coalition participating in sanctions against Russia accounts for more than 90% of global currency reserves, approximately 80% of global investment, and 60% of world trade and economic output. In a world where economic relations increasingly have security overtones, the 60-plus countries under the US security umbrella are likely to stick with the dollar even if they oppose Western sanctions.

The stakes are high. If a multipolar currency order was imminent, it would be reasonable to call for a reversal of US monetary, spending, and sanctions policies. But for the time being, the better bet is on continuing dollar dominance.

No comments:

Post a Comment