Source Link

Although the roots of the European Union lie in economic integration, the EU’s economic policy competences and possibilities are narrowly limited in European primary law. Nevertheless, the influence of the EU, and in particular the European Commission, on economic policies of the member states is clearly visible and tangible.

The focus of European economic policy is on the coordination of member state policies by the European Commission. It uses strategic planning instruments such as 10-year strategies, guidelines, and reform recommendations, which it bundles within the European Semester.

European economic policy-makers are actually faced with the task of limiting the acute socio-economic consequences of the Covid-19 pandemic on the one hand, and finding answers to the structural challenges posed by globalisation, digitisation, and climate change on the other. A common European economic policy is becoming increasingly necessary, and expectations are growing.

The European Commission is trying to combine these two tasks – the stimulation of the European economy and the sustainable transformation of national economies – with the new European recovery fund “Next Generation EU”. The European Green Deal will become the guiding principle for both economic policy coordination and economic policy at the national level.

This reorientation of European economic policy towards sustainable and decarbonised growth will promote the Europeanisation and, in the long term, the unitarisation of national economic policies.

Issues and Conclusions

One of the roots of the European Union (EU) and a major driving force behind the process of European integration was, and still is, the integration of national economies into a common market with a common currency. European unification has always been an economic project. This makes it all the more surprising that the EU is not actually allowed to pursue an independent economic policy. The European treaties do not provide for this. Instead, the member states can only coordinate their respective economic policies in the common interest. Nevertheless, even the EU can fall back on an economic constitution and order, and it undoubtedly has its own instruments for implementing its economic goals.

In view of this starting position, two sets of questions need to be answered:

1. What are the guiding principles and objectives of European economic policy? What are the EU’s current competences and possibilities, and how does the Union, and in particular the European Commission, use its economic policy instruments?

2 What will European economic policy look like in the new decade? What new economic goals are moving into the EU’s focus, and how could this policy evolve in the long term?

An analysis of the policy field, tasks, and options of European economic policy should start with a description of the competences transferred to the EU by the European treaties and the existing policy instruments. It is only against this background that it becomes apparent how far actual European economic policy has distanced itself over the past decade from the legal foundation of the policy, which is still formally dominated by the EU member states.

The EU has limited economic policy options, but it has used its instruments effectively and successfully expanded its room for manoeuvre over the last decade. This is particularly true of the European Commission. Although still formally dominated by the EU member states, it has made skilful use of its room for manoeuvre to initiate a steady process of Europeanisation and supranationalisation of economic policy. This is an approach that will continue with the European Green Deal and as part of the joint response to the socio-economic consequences of the Covid-19 pandemic. If this trend continues in the long term, further unitarisation of European economic policy can be expected.

However, whether it will be possible to switch to a sustainable and climate-protecting form of economic activity throughout the EU under the conditions of digitisation, as envisaged, depends on whether the structural and systemic limitations and obstacles to an active, coherent, and efficient European economic policy can be removed. To this end, the EU should be equipped with additional economic policy instruments, such as an extended competence for fiscal policy issues, so that the Community can provide effective economic policy incentives through the price mechanism. However, this can only be achieved by amending the European treaties, that is, gaining the consensus of all member states – which is currently not in sight. Transferring additional powers and adapting the European treaties is therefore a rather long-term objective.

The central instrument of European economic policy is the European Semester: a framework for policy-making and steering with fixed deadlines for evaluation, recommendations, and implementation; it brings together and takes into account all economic, employment, social, and, in the future, sustainability policy goals and strategies of the EU. The reorientation of the European Semester towards global challenges should not, however, lead to an overloading of this central steering instrument. The economic policy objectives should remain at the centre, that is, monitoring macroeconomic and fiscal policy in the member states and implementing economic policy reforms to enhance competitiveness and create jobs. Under the conditions laid down in the EU treaties, the European Semester is the only instrument that enables effective economic policy coordination of the member states: by focussing on common objectives and interests, through financial incentives from European funds and – under certain conditions – through sanctions in the event of non-compliance with the jointly agreed economic policy. Overloading the European Semester with additional objectives and topics should therefore be avoided, as this would threaten to undermine the political objectives and make them less clear. This could possibly take away the relevance and urgency of the Commission’s recommendations for economic policy reform.

The European single market must remain at the heart of European economic policy. The European social market economy requires open markets and free competition. Considerations of politicisation, particularly of European competition and state aid control, or protectionist restrictions on access are therefore not appropriate. The reactions of member states at the beginning of the pandemic have shown how quickly and far-reaching protectionist measures can hinder and slow down the exchange of goods, services, and people in the European internal market. The very essence of European integration would be put at stake. The economic power of the internal market and the EU’s regulatory strength will only be effective and convincing to global competitors if European economic policy respects the foundations and framework of its own economic constitution.

The Foundations of European Economic Policy

Economics and politics are closely interwoven; the decisions made in political institutions influence economic decisions; conversely, the economic situation and its development affect political preferences and priorities.1 The task of economic policy in a heterogeneous environment with differentiated interests is to find an appropriate balance between the individual interests of economic actors, the overall welfare, and other political and social objectives. In the EU, general economic policy ranges from employment and social policy to consumer protection, infrastructure, tourism, and industrial policy.2

Consequently, the fields of action of economic policy are both the development of structures of the economic order and questions of steering and regulating economic processes and decisions. For this reason, a distinction is usually made between the more structural, long-term, and normatively-oriented policy for the creation and shaping of an economic order and economic constitution – which essentially maps and concretises the decision of a community on its economic system – and the more short- to medium-term economic process policy, which is primarily determined by the day-to-day political decisions of the government.3 An economic constitution creates the normative foundations of the respective economic system of a state and provides the economic constitutional foundations, which define the framework of the respective economic system and the rights and obligations of public and private economic actors. In essence, the economic constitution is the economic system decision of a community and its constitutional concretisation.

Under the special conditions of the EU’s multi-level political system, the scope for action for both elements of economic policy is limited, even though the need for a coordinated and effective common European economic policy has become clear to all actors, at the latest with the creation of the single European market in the early 1990s and the single currency. The respective understanding of form, content, task, and objective of European economic policy still differs among the member states. Despite all the pleas for a deepened “European economic union for convergence, prosperity and social cohesion”,4 the European Commission concluded as late as 2017 that European economic policy will lag behind national economic policies, particularly in the euro zone.5

The European economic constitution: The leitmotif of the social market economy

At a very early stage, Ernst-Joachim Mestmäcker considered the application of the term “economic constitution” to the process of European integration to be justified since the Treaty of Rome in 1957.6 Since then, the European economic constitution has been based on free competition between economic actors in a common market for the exchange and trade of goods, services, capital, and persons. The creation and safeguarding of open markets in which undistorted competition prevails were – and are – undoubtedly constituent elements of a market economy. However, this model was initially lacking in the European treaties and therefore repeatedly questioned with reference to interventions in market mechanisms in agriculture and coal and steel. The respective ownership systems in the member states initially left the European treaties untouched and open. It was only with the Maastricht Treaty in 1992 that the member states and the Community committed themselves to the principle of “an open market economy with free competition”,7 a commitment that was finally supplemented and reworded by the Treaty of Lisbon in 2007. Article 3 of the Treaty on European Union now refers to a “highly competitive social market economy” that should also aim at full employment and social progress.8 The Treaty of Lisbon also incorporated the Charter of Fundamental Rights of the European Union into European primary law. Its articles – entrepreneurial freedom, the right to property, and collective fundamental rights such as the right to access to a job centre, protection against unjustified dismissal, and the right to social security and assistance – became part of the European economic constitution and the model for a social market economy.

Many fundamental economic policy decisions and structures in Europe can be traced back to regulatory policy ideas of the Federal Republic of Germany.

The shaping of the European economic constitution was influenced by the ideas9 of the Federal Republic of Germany, especially those of Walter Eucken and the Freiburg School. To this day, ordoliberal principles and structural decisions can be seen in day-to-day European economic policy decisions, for example in the measures that the EU has been using in response to the deep crisis in the euro zone since 2011.10

With the process of European integration and the penetration of national economic systems by European legislation, the scope for differences in national economic constitutions has become noticeably narrower.11 European fundamental freedoms in the internal market, supranational competition, and state aid law and Community regulations set the framework for national economic policies and economic constitutions.12

The limits of European primary law

Nevertheless, European economic policy is still dominated and determined by EU member states. Like the founding European treaties, the Treaty of Lisbon – in Article 119 of the Treaty on the Functioning of the European Union (TFEU) – speaks only of “close coordination of member states’ economic policies”, based on “the internal market and the definition of common objectives”. The member states are to regard their economic policies as “a matter of common concern” (Article 121 TFEU) and direct them towards common objectives.

The European treaties do not provide for supranational economic policy.

European primary law clearly provides no legal base for supranational economic policy-making. The member states have so far always rejected any transfer of economic, employment, or social policy competences to the EU that would go beyond the present level and allow the harmonisation or centralisation of policies. The obvious contradiction between the retention of national sovereignty and the need for Community action on these very policies is to be resolved by the softer method of policy coordination.

Consequently, the responsibilities for economic policy-making are those that have either been transferred only in part to the EU or remain entirely within the competence of the member states. In any case, equipping the EU with the appropriate political and legislative instruments to implement an efficient and coherent economic policy has its limits in the division of competences between the EU and member states. Thus, the EU is denied a central instrument of national economic policy: the levying of taxes or the modification of existing tax rates. As a result, an important channel for influencing the price mechanism in the European internal market is lost.13 The few tax policy competences of the EU in the field of indirect taxation are primarily intended to ensure equality of competition and compliance with the prohibition of discrimination in the European internal market. The consensus-based harmonisation of indirect taxation is only possible “to the extent that such harmonisation is necessary to ensure the establishment and functioning of the internal market and to avoid distortions of competition” (Article 113 TFEU). Although the harmonisation of direct taxes, in particular corporate tax, and the establishment of a uniform basis of assessment have also been discussed for several decades, the Commission has not yet reached a consensus on the need to harmonise indirect taxes. However, these initiatives are also limited to the objective of ensuring the equality of competition in the internal market. A genuine economic governance effect with a Community tax policy has so far played only a minor role in these debates.

Internal market, competition policy, and monetary union

From the outset, European integration was intended to create a common market for goods, labour, capital, and services with a level playing field and the establishment of a customs union. Both were to be achieved through a policy of legislative approximation and standardisation. Harmonisation covers framework conditions, production, and product specifications, but also the rights and their protection of market participants, which are addressed, for example, by consumer and labour protection legislation. Because of the large number of national laws to be harmonised in addition to the technical and administrative obstacles, the principle of harmonisation was supplemented by the principle of mutual recognition at the end of the 1980s in the course of the European Commission’s internal market programme and the Single European Act. The regulation of the internal market and its four market freedoms by means of European legislation is still the central economic policy instrument of the EU today. It is also intended to achieve economic convergence.

The common economic area can only function in the long term if restrictions of competition by companies or public authorities are eliminated.14 As a supranational institution committed to the European common good, the European Commission acts as the European competition authority – irrespective of the national or regional interests of the member states. It is responsible for the competition law categories laid down in European primary law, namely the prohibition of cartels; other restrictive measures or agreements; mergers and abuse of a dominant market position; as well as for monitoring the basic ban on state aid and monitoring of public tenders. However, the strict European competition and state aid policy is in tension with other forms of European economic policy. This applies in particular to European support programmes for the agricultural sector and – with the help of the Structural Funds – for regions, to European industrial policy, but also to the special handling of services of general interest such as energy supply, telecommunications, and local public transport.

The Maastricht Treaty set a constitutional objective of economic integration that went beyond the single market: the creation of the European Economic and Monetary Union. A supranational monetary and exchange rate policy in the euro zone was intended to complement and enhance the EU’s more narrowly focussed economic policy, which was geared towards completing the single market. Even in the run-up to the Maastricht negotiations, there had been intense and controversial debate about whether a common economic policy was indispensable for the stability and functioning of monetary union. Finally, it was agreed that the necessary economic convergence in the euro area would be achieved through a deeper economic policy coordination of national policies. The transfer of competences and responsibilities for monetary policy to supranational bodies was deliberately not reflected in economic policy. In contrast to the scope and objectives of the single market-related European economic policy, supranational monetary and exchange rate policy is primarily geared to macroeconomic and macro-financial aspects: The member states must keep their national public budgets permanently stable and are obliged to avoid excessive public deficits.

The two elements of European Economic and Monetary Union – economic policy on the one hand, and monetary and exchange rate policy on the other – are therefore different. There are considerable differences both in terms of their binding force under primary law and in terms of the political and legal instruments available to the EU and its institutions. This discrepancy has consequences: for the scope of member states’ fiscal policy and the EU’s ability to exert influence.15

European economic process policy

Although the EU’s legislative powers in the field of economic policy are clearly limited by primary law, the EU and its institutions have developed a comprehensive and far-reaching economic process policy – with an only modest set of instruments, which is also limited in its scope.16

Instruments

The policy is not entirely outside the EU’s competence. The role and influence of the European institutions in supporting instruments such as the Broad Economic Policy Guidelines (Article 121 TFEU) are laid down in the treaty; but the European Commission in particular can develop its own ideas on the topics and objectives of coordination, and thus set its own priorities as an agenda setter.17 In principle, the EU has the following four instruments at its disposal for shaping a European economic process policy.

Legislation and regulation of the internal market

The EU can regulate the internal market with European legislation, albeit not fully and completely autonomously. Legislation harmonising national regulations and European competition and state aid law are of particular importance in this respect. In addition, the Union has powers for certain sectors, such as agricultural and fisheries policy, energy policy, transport policy with trans-European networks, and related policy areas such as consumer protection and environmental policy.

The EU’s regulatory activity can open up new markets for the internal market and European competition or expand existing ones. The Services Directive for the services sector, the Capital Market Union for the financial markets, initiatives in traffic and transport policy, the energy sector and public resp. universal services are well-known examples. The EU is now also aiming for a single European market for data, given the growing importance of digitisation.18

The opening of markets to free competition, that is, deregulation, often entails both the possibility and necessity of re-regulation. This means more than mere legislation. Specifically, it involves setting limits or standards, monitoring them and, where appropriate, imposing sanctions in the event of non-compliance, and creating or establishing appropriate procedures and institutions – in other words, clearly the exercising of an economic process policy.

Enforcement of European competition policy

As the European Commission is the European competition authority, it can intervene in the market by specifying the competition and state aid requirements of European contract law, regulating implementation, and monitoring compliance. The Directorate-General for Competition is responsible for the preparation and processing of specific competition-related cases and for the investigation, evaluation, and preparation of decisions such as fines, merger prohibitions, and company splits.

The Commission cooperates closely with the national competition authorities in a European Competition Network and usually intervenes only when a potential infringement of European competition law affects several member states or companies in several member states.19 However, the Commission is empowered to assume jurisdiction in an individual case and submit opinions to the national courts on its own initiative if it has concerns about the interpretation of national authorities. Its interpretation of how European competition and state aid law should be applied and the case law of the European Court of Justice (ECJ) can guide decisions at the national level. It also provides guidance on areas of application of European competition law in order to ensure consistency in the application of the law and the conformity of decisions on competition law with judgments of the ECJ.20

Community objectives and policy coordination

In areas where there is no legally binding regulation, the EU nevertheless has the possibility of influencing the framework, priorities, and measures of member states’ economic policies. By proposing common objectives at the European level that are accepted and implemented by the member states, the EU can set politically binding priorities and guidelines. However, implementation and, in some areas, the choice of appropriate measures will remain the responsibility of the member states. Economic policy coordination involves competition between countries to find the best way to achieve the commonly agreed objectives, promoting mutual learning between member states, and comparing national policies and models. The EU, usually the European Commission, may also be mandated by the member states to monitor and, if necessary, sanction compliance with – and implementation of – commonly agreed objectives and targets. It can thus at least indirectly influence economic developments in the EU and the member states and exercise some economic policy control.

Financial incentives and conditionalities

The EU has a small budget compared to member states’ budgets, and its autonomy in using these financial resources is limited. However, it can provide effective start-up financing through its own funds and investment or support programmes, and it can combine this with conditions for implementing policies and objectives.

The Common Agricultural Policy (CAP) is the oldest, best-known, and most criticised EU support policy for a specific sector of the European internal market.21 For the so-called first pillar of the CAP – direct payments to farmers and market support measures – a total of €278 billion (at 2011 prices) has been earmarked for the current financial period 2014 to 2020. The second major area of expenditure from the EU budget comprises the European Cohesion Funds and Structural Funds; in the current funding period, a total of €325 billion is available to boost growth and employment.22 If the necessary national co-financing is added, these funds provide the EU with a powerful economic policy instrument worth around €650 billion.

In addition, the EU has the possibility to co-determine member state and regional funding priorities through the specific legislation and its Cohesion Policy steering and planning documents. A “paradigm shift” has taken place: away from transfers and their distribution, and towards growth and results-oriented investments.23 There is no doubt that European Cohesion Policy and the Structural Funds have now become the main financial instrument of European economic policy. The EU offers similar incentives to other sectors of the economy, either directly through the creation of favourable framework conditions, or through accompanying member state policies. There are, for example, programmes to build up and expand infrastructure; promote individual industrial sectors, especially small and medium-sized enterprises (SMEs); support innovation and research; in addition to education policy support programmes.

With the help of its own institutions, such as the European Investment Bank (EIB), the Union can also supplement its financial incentive policy with loans and guarantees.

European Economic Policy-making

The EU’s economic policy instruments therefore consist primarily of policy coordination and coordination of the economic policies of the member states. The European Commission can only fulfil this task, which is laid down in the European treaties, after first ensuring that there is a common understanding of the economic challenges that the member states want, or should, tackle together and which political objectives are derived from this assessment.

With the help of strategies and guidelines drawn up and agreed upon for this purpose, the EU, and in particular the European Commission, is perfectly capable of influencing the economic policies of the member states. In agreement with the member states, it can define the objectives of – and priorities for – their economic policies, set or change the framework conditions, and monitor compliance with the principles laid down in the European economic constitution: the safeguarding of free and unrestricted competition in the common market.

Regulation of the internal market

The internal market is at the heart of economic integration, and thus also of European economic policy.24 Around 520 million people currently live in the enlarged internal market. As this integration project is never complete, the internal market must be continuously adapted and developed to meet the challenges of a changing environment and new circumstances.25 Its economic and political importance is immense; it is “one of the greatest achievements of the European project [...] it has been instrumental in increasing the prosperity and wealth of the citizens of the European Union”.26

With the economic power of the internal market, the EU is able to externalise its own standards, norms, and rules.

This economic power of the internal market enables the EU to externalise its own standards, norms, and rules and enforce them globally.27 With its competition policy in particular, the EU can achieve international regulation that extends beyond the Community on the basis of European competition law28 and – using the “Brussels effect” smartly – triggers a real race to the top in the competition for standards in consumer and labour protection as well as in social, environmental, and employment policy. This global expansion of high European standards and requirements could be successful primarily if the EU reacts quickly, distinctly, and in a strictly regulatory manner to attempts by global competitors – but also European suppliers – undermining EU rules.

Digital policy is a good example of the new regulatory tasks. When innovation creates new markets, the EU is called upon to draft directives and regulations for the internal market and access to it. The regulation of the data markets in particular shows the scope for regulation, which goes hand in hand with the EU’s immense market power. The General Data Protection Regulation is certainly the best-known example of “Europe’s regulatory model” and acts as a “strong reference point for many outside Europe”.29 With the new digital and data strategy, the Commission also aims to reinforce “Europe’s ability to define its own rules and values in the digital age”.30

The EU also has a similar level of market and regulatory power concerning high product standards and environmental protection laws.31 Against the background of global trade conflicts and its ambitious climate and sustainability objectives, the EU is also working on adapting its strategic planning documents, agendas, action plans, as well as the objectives and measures set out in these in order to increase its ability to externalise European standards. The political use of the “Brussels effect” now extends beyond the mere protection of European consumers and producers and increasingly endeavours to extend European values, political objectives, and global standards, such as the protection of universal human rights as well as environmental and climate protection measures. As part of the European Green Deal, the Commission intends to encourage the EU’s international partners in the future “to design similar rules that are as ambitious as the EU’s rules, thus facilitating trade and enhancing environment protection and climate mitigation in these countries”.32 The European internal market is increasingly developing to serve the EU’s value-based international policies and interests.33

EU member states benefit from the internal market and Customs Union in two ways: through the advantages of trade with third countries and through the benefits for their own economies. On the one hand, the common market provides external security and strengthens the position of member states in global competition. On the other hand, various studies have shown that trade between countries in the internal market has also increased significantly, especially since the major enlargement round in 2004 with the accession of eight Central and Eastern European countries. The Commission calculates that the annual benefit from integration into the internal market for the EU-27 member states is almost 6 per cent of gross national income (GNI), or €923.6 billion.34 Although the studies evaluated by the Commission show that the positive effects of market integration are unevenly distributed between member states and regions, they nevertheless show that the internal market is worthwhile for all member states.

The alignment of the regulatory density and depth of the four market freedoms is an ongoing task.

There are also differences in the density and depth of regulations, both in terms of the four market freedoms of the internal market as well as public procurement. Divergences still exist between markets for goods and services, and these are reflected in the volume of intra-European trade. Whereas the internal market for services in the EU-28 was responsible for an average of 4.7 per cent of GNI in 2017, the exchange of goods contributed 19.6 per cent to GNI.35

The transposition of internal market directives into national law is of great importance for the legal certainty of all market participants. According to a list36 drawn up by the European Commission, by 1 November 2019 a total of 1,083 internal market directives37 had been adopted that were – or are still to be – transposed by national legislators.38 The Commission regularly monitors compliance with the transposition deadlines, because if European legislation is not transposed within the prescribed time frame or is transposed incompletely, the internal market gradually loses coherence and significance. The Commission sets margins and publishes the results in an annual scoreboard.39 Only a maximum of 0.5 per cent of EU internal market legislation in individual member states is not transposed, or transposed too late or incompletely.40 The Commission’s Internal Market Scoreboard 2020 provides an overview of the state of the transposition of directives in the individual member states, and the degree of openness and integration of the markets for 2019, showing that the average EU transposition deficit was 0.6 per cent of all directives, with an average delay of 11.5 months; the conformity deficit was 1.2 per cent.41 The latter refers to the difference between de jure and de facto transposition. One indicator of this disparity is the infringement proceedings that the Commission launches against a member state for the incorrect transposition of a directive. Although the number of proceedings recently has increased slightly, in the long term it has been reduced from a peak in 2007/08.

A decade ago, Mario Monti had already made proposals for adapting the single market to new economic, employment, and sustainability challenges in a report named after him.42 The Commission responded with a number of initiatives.43 These strategies with packages of measures to further develop the single market were followed by sector-specific and market-opening legislative proposals for an Energy Union, a Banking Union, and a Capital Market Union. This essentially horizontal approach of the Commission is complemented by analyses and strategies for individual sectors of the economy, ranging from the automotive, space, and chemical industries to the social economy.44 With this sectoral approach accompanying the policy, the Commission is attempting to focus more strongly on the horizontal objectives of competitiveness and the capacity for innovation and adaptation of a common internal market policy.

Member states took up the Commission’s proposals and sought to integrate the wide range of initiatives, strategies, action plans, and individual measures into an overall coherent strategic economic policy approach. The spring European Council on 21–22 March 2019 identified the deepening of the European Economic and Monetary Union and the internal market, a strong industrial policy, a forward-looking digital policy, and an ambitious and robust trade policy as elements of this “integrated approach”.45

Competition law and industrial policy

In the field of industrial policy, the European Commission is also focussing on the development of strategies to arrive at a common understanding of future guidance and challenges. A paper that was presented in 2017 to prepare the EU for the “new industrial age” and launch a “holistic and forward-looking vision for Europe’s industry”46 was followed by a proposal for such a vision in 2020. In the coming decade, the sector must become greener, more sustainable, and digital, all while maintaining its global competitiveness and social sustainability. As with its previous strategy papers, the Commission avoids direct intervention and limits itself to improving the economic framework conditions for industrial enterprises and accompanying activities. The aim is to support the digitisation of industry and the internal market, and to promote initiatives to achieve climate neutrality and a CO2-saving recycling economy. Through industrial innovation and the expansion of research and development programmes, Europe’s industrial and strategic autonomy is to be strengthened and the development of key technologies supported. In addition to these IPCEI (Important Projects of Common European Interest) – for example in robotics and microelectronics as well as biomedicine and nanotechnologies – European value chains or “industrial ecosystems” should be developed. The use of foreign direct investment should be examined more closely than in the past.47 With this new strategy, the Commission confirms its more business-supporting and framework-based approach to influence European industrial policy by agreeing on common objectives. For key technologies only, the Commission proposes individual measures to provide an impetus or incentive, such as investment in the development of batteries to meet low-emission mobility targets.

In addition, some member states support EU industrial policy measures. Following a French initiative, a group of 20 member states has been meeting regularly since 2013 to coordinate their national industrial policies as “Friends of Industry” and agree on common objectives and measures. The member states have now agreed on agenda-setting objectives for the internal market and a European industrial policy, as well as measures to boost the growth and competitiveness of the European economy. In addition, there were initiatives to modernise European competition policy and develop accompanying policies, such as education and research policy, support for SMEs, and measures to promote sustainability and climate protection.

In principle, European industrial policy creates opportunities to intervene in existing or emerging product markets – and is thus inevitably subject to tensions with European competition, anti-trust, and state aid law and the European rules on public procurement, which are monitored by the Commission. The Commission’s neutrality – or that of the responsible Directorate-General for Competition – ensures that decisions are accepted and thus applied. The Commission is extremely positive about its work: “The predictability and credibility of the EU’s system has made the Commission one of the leading and most influential competition authorities in the world.”48

A reform of competition policy should make “European champions” possible.

However, Germany, France, and Poland are now questioning the Commission’s prominent role as a competition authority and calling for a comprehensive reform of European competition policy. New global challenges require:

a) an adjustment to the changing international competition in which those companies, in particular from China, with state support may distort fair competition;

In summer 2019, the German, French, and Polish ministries of economic affairs presented proposals – Berlin linked its initiative for a national Industrial Strategy 2030 to the European debate.50 The three ministers called on the Commission to modernise its guidelines for mergers in order to be better able to deal with takeover attempts by state-controlled companies from third countries in the European market, and to examine more efficiently and quickly whether – and to what extent – large international tech groups are abusing their dominant positions. By merging European companies, they want to enable the creation of “European champions” in order to remain globally competitive.51 The three member states also called for a political assessment of issues regarding competition law. In the Competitiveness Council (COMPET) the ministers should be able to discuss and influence the Commission’s actions, down to the level of individual decisions, and even annul decisions if necessary. The aim of this trio-initiative is, in addition to responding to the new global challenges facing European competition policy, to limit the Commission’s dominant role in the interpretation and application of competition law. However, this objective is by no means shared by all member states. The Dutch government, for example, in a separate position paper, advocates maintaining and further strengthening the political neutrality and independence of European competition policy.52 The far-reaching objectives of the trio and the criticism of the Commission will therefore have to be discussed further among the member states.

In addition, the application of European competition law by the Commission and the national competition authorities, as well as its interpretation by the ECJ, is by no means purely inflexible or unadaptable and, as claimed, has left the changing political environment unrecognised. Instead, general economic policy objectives are also taken into account; there is therefore room for adjustments and policy changes. In particular, the European Commission’s greater consideration of economic and consumer protection concerns and consequences in the application and interpretation of European competition law, which has remained virtually unchanged, has led since the 1990s to an “economic approach” to European – and subsequently also member state – competition law and its application.53

Strategic planning and economic policy coordination

The EU has only limited scope for economic policy regulation. As a driving force and agenda setter, it – and in particular the European Commission – must try to commit the member states to common objectives in the course of economic policy coordination. European economic process policy therefore usually begins with the preparation of planning and strategy documents, which helps to bring the different approaches of member states closer together. The aim is to develop a common understanding of problems, challenges, and objectives. In the best case, this process ends with the agreement of a coordinated sequence of steps for Community reactions and measures. The main purpose of these planning and strategy documents is thus to define and specify the matters of common interest identified in Article 121 TFEU and, in the course of coordination, to derive the appropriate measures for the economic policies of member states.

The EU’s economic policy strategies provide the reference framework for coordination between member states.

Since the 1990s, the Commission has endeavoured to develop the economic process policy for which it is responsible and to make it more effective and target-oriented.54 Since 2000, it has used multi-annual growth strategies, starting with the so-called Lisbon Strategy,55 which was replaced by the Europe 2020 strategy in 2010. The strategies have provided the reference framework for the coordination of all strategic initiatives and the many economic policy coordination processes that have been launched in the EU. With these 10-year strategies, the Commission succeeded in circumventing the limits of its influence on the economic, employment, and social policies of the member states, which are anchored in primary law: The real political value of the strategies was that they provided new instruments for economic policy-making agreed between the Commission and the member states. The real task was not the implementation of the reform objectives, but the development of an ever closer, more efficient, and then sanctions-based coordination process.56 The Europe 2020 strategy also made use of this soft form of economic policy-making. However, the focus shifted to fundamental macroeconomic issues to stabilise the euro area. To this end, the open method of coordination was replaced by a new coordination instrument: the “European Semester”.

The Juncker Commission refrained from presenting a new 10-year economic policy strategy. The new European Commission under Ursula von der Leyen, however, took over this task with the European Green Deal. With this “new growth strategy” for the coming decade, it hopes to “develop the EU into a fair and prosperous society with a modern, resource-efficient and competitive economy”.57

The European Semester

Since 2011, the European Semester has been at the centre of economic policy coordination in order to more closely interlink the diverse coordination and agreement processes in the individual policy areas.

It usually starts in November with the presentation of a comprehensive so-called autumn package.58 In the EU Annual Growth Report, the European Commission analyses the economic situation in the EU and the euro area and presents its forecast for the following year, supplemented by draft reports on the implementation of the Broad Economic Policy Guidelines and the Employment Guidelines, as required by the TFEU. In addition, the Commission provides assessments of the member states’ stability and convergence programmes and, since 2012, an early warning report on their macroeconomic imbalances. On the basis of these analyses, the European Commission proposes economic, employment, and social policy priorities for action for the EU and the euro area. The member states examine the proposals, in particular in the Economic and Financial Affairs Council (ECOFIN), the COMPET, and the Employment, Social Policy, Health and Consumer Affairs Council (EPSCO). Meanwhile, the Commission prepares the so-called Winter Package: a separate country report for each member state in which it analyses and evaluates the economic, employment, social, and budgetary policy decisions and measures over the past year and compares them with the common European objectives and the Union’s reform recommendations for member states. These recommendations for measures and reforms are derived from the progress or problems of the member states and presented by February of the following year.

Figure 1

The relevant Councils also examine and discuss this package and then submit their own assessments and recommendations for guidelines to the European Council. At their spring summit in March, the heads of state and government agree on economic and employment guidelines, which must then be implemented at the member state level, together with the country reports and the so-called Country-specific Recommendations (CSRs). Member states draw up National Reform Programmes (NRPs) and, with regard to their budgetary policies, their stability and convergence programmes or, if they are not yet members of the euro area, convergence programmes on their medium-term budgetary policy-making. In these programmes, they set out in detail the measures they plan to take, the objectives they want to achieve, and how they intend to remove obstacles to sustainable economic growth. These NRPs are thus the member states’ counterparts to the European recommendations for economic and employment structural reforms. They must be received by April by the Commission, which analyses and assesses them. The overall package of Commission forecasts and country reports, Council opinions, European Council guidelines, and National Reform and Stability or Convergence Programmes forms the basis for the CSRs. As precisely formulated guidance, they provide the member states with guidelines for continuing, intensifying, or refocussing their national structural reforms. The member states also examine and discuss these Commission recommendations in the Council formats involved and adopt the final reform recommendations by July – to be implemented by the member states in the second half of the year, the national semester. The Commission’s next autumn package is then launched during the next cycle of the European Semester in November.

The European Semester: fixed tasks, fixed procedures, modest progress so far.

The European Semester is thus the organisational and administrative clamp with which the European initiatives and instruments for closer economic policy coordination have been held together, synchronised, and extended beyond the limited economic policy area since 2011. It provides the formal and substantive framework for direct coordination and cooperation between the European Commission and the governments of the member states on almost all issues of financial, budgetary, economic, employment, and social policy.

The country reports also encourage bilateral exchanges between the ministries concerned in the member states and the Commission services on indicators, findings, and conclusions as well as on the necessary, possible, and promising structural reforms. The European Semester thus serves the development of the member states as well as the development of a common understanding of economic policy-making.

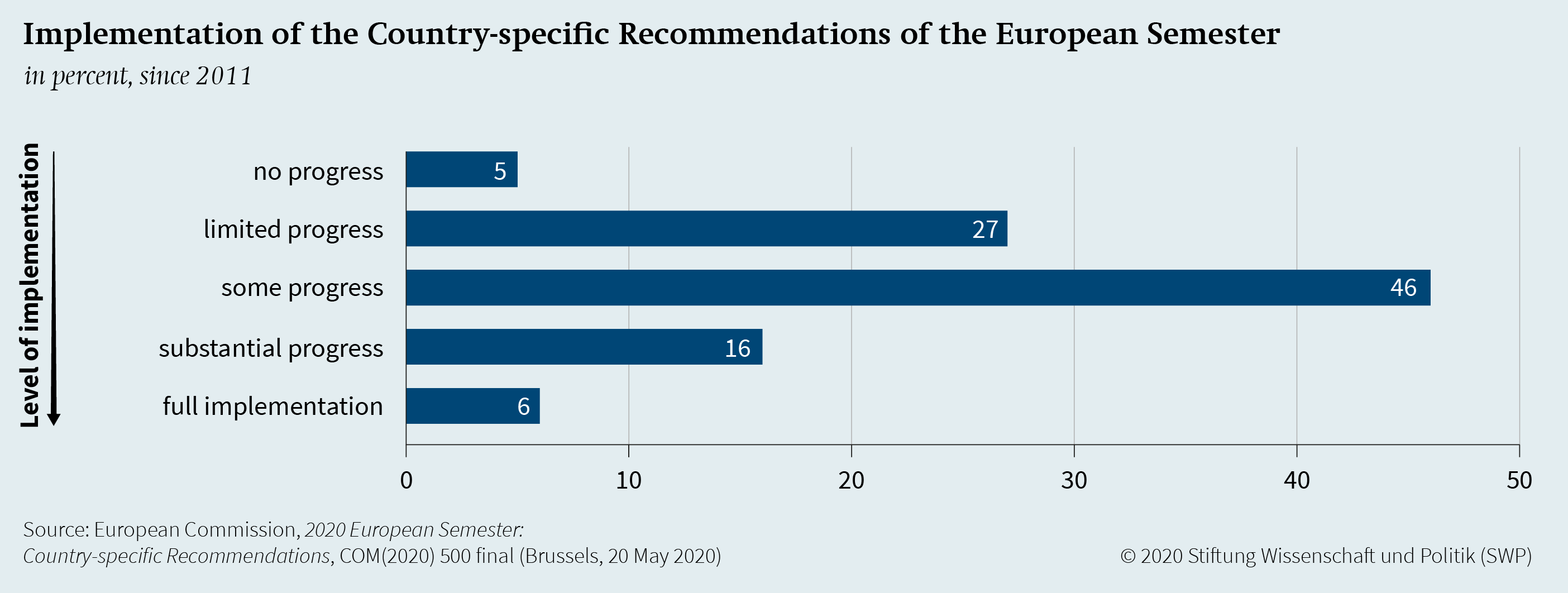

However, the implementation of the CSRs has not been convincing so far.59 The evaluation annually presented by the Commission shows that since 2011, only 6 per cent of these recommendations have been fully implemented, while 16 per cent have made considerable progress; 5 per cent of the CSRs have not yet been tackled. The most serious desiderata were to be found in the areas of competition in the services sector and long-term sustainability of public finances (including pensions).60 The Commission also had to admit that in some cases “there is evidence of backtracking on elements of major reforms adopted in the past”.61 In principle, however, this list is purely statistical. It does not rank priorities or distinguish between more important from less urgent CSRs.

For Germany, the Commission stated in its country report for 2020 that at least “some progress” had been made in 54 per cent of the reform recommendations, but only limited progress in 46 per cent. “Compared to 2014–2017, Germany’s implementation of CSRs has improved recently, though only to a limited extent, and is now roughly in line with the average progress made by other member states.”62

Country-specific reform recommendations became de facto implementation guidelines.

Although it is the European Council that takes note of the Commission’s analyses as well as growth and employment reports in the spring; formulates its own broad guidelines for the European Semester on this basis; and finally adopts the CSRs, the European Commission dominates the European Semester.63 The recommendations are proposed by the Commission, and the member states can only deviate from this line that the Commission proposes and push through changes in the Council if the latter approves the changes to the Commission proposal with a qualified majority. The comply or explain rule in particular makes it difficult for member states to simply reformulate, water down, or even delete the Commission’s CSR formulations. According to this rule, the Council must either adopt the Commission’s proposals or publicly explain and justify changes in a separate opinion.64 This significantly enhances and strengthens the role of the Commission. Some observers speak of “small self-empowerment by the Commission”.65 Recommendations have become de facto implementation guidelines for the member states.

Thus, the European Semester first of all strengthens the role and influence of the European Commission in the intergovernmental coordination of economic, fiscal, and employment policies of the member states.66 However, the Commission is relatively cautious and reserved in its recommendations for those member states where the need for reform is great but the willingness to do so is, for a variety of reasons, low.

If member states wish to influence the EU recommendations under consideration, informal discussions between the ministries of a national government and the Commission prior to the adoption and publication of the recommendations are the most appropriate way to do so. The Semester therefore allows – and even forces – close coordination with the Commission. “Member states do not control the European Semester, nor have supranational institutions become all-powerful.”67 Instead, a relatively efficient interaction between the European and national executive authorities seems to be developing to tackle reforms and remove obstacles to reform in the common interest in the member states.

Nevertheless, the role of the European Commission in this coordination process has been significantly enhanced. It can now influence and steer national economic policies – as the hub of economic policy coordination. The soft coordination that used to be based on Community targets and non-binding recommendations is now giving way to a markedly stronger economic and reform policy-making with an increasingly European character and with centralising and harmonising approaches. This trend will continue with the new growth strategy: the European Green Deal.

Incentives through funding

With the help of the European Semester, financial incentives through European funding policies serve as important supplements to European economic policy-making. The Structural Funds are the focus here: For some years now, they have been slowly but increasingly developing into an important economic policy steering instrument of the EU with a “clear investment strategy in every region”.68 The soft medium- to long-term goals of the 10-year growth strategies and the short-term reform priorities in the course of the European Semester can be tightened up with the instruments of conditionality.69 In the current Cohesion Policy funding period 2014 to 2020, this took the form of so-called macroeconomic conditionality. This form of conditionality, which is still highly controversial today, links the disbursement of money from the Structural Funds to compliance with the EU’s economic policy guidelines and CSRs.70 The Commission can ask a member state to change its funding priorities so that the European Structural Funds serve the common economic policy objectives and the implementation of CSRs in the context of the European Semester. It may also suspend all or part of the commitments and payments of Structural Funds if a member state fails to comply with the guidelines and recommendations of economic policy coordination.

The Structural Funds will increasingly serve an evolving European economic process policy.

Additional strategic planning and control instruments in the structural policy support programmes of the regions – such as the Common Strategic Framework and the conclusion of Partnership Agreements between each member state and the European Commission – also ensure that priorities, recommendations, and reform goals become binding guidelines beyond the division of competences in the European treaties. This form of “soft influence”71 enables the Commission to examine and enforce compliance with economic, financial, employment, budgetary, and social policy objectives and guidelines. The European Structural Funds no longer just serve to promote intra-European solidarity between prosperous and poorer regions, but are increasingly becoming policy-making instruments of an evolving European economic policy. This change in function is also evident in the fact that all regions in the EU are now eligible for funding, in principle. This steering or push-effect of European funding policy will be further enhanced in the funding period 2021 to 2027. The European Commission’s claim to control is becoming increasingly apparent.

European economic stabilisation policy: The EIB and the Juncker Plan for strategic investments

Between 2007 and 2014, in response to the deep euro crisis, the volume of credits by development banks in the EU increased sharply. Both the EIB and the national development banks gained in importance as economic policy actors,72 as they took on the task of initiating an anti-cyclical economic policy by means of investment promotion.73 This made close cooperation between the EIB – which increased both its share capital and its investment capital – and the European Commission essential, “bringing the two institutions closer together”.74

The Commission, under its then-President Jean-Claude Juncker, pushed ahead with the EIB’s involvement in its economic policy initiatives. With the European Fund for Strategic Investments (EFSI) – the so-called Juncker Plan for Strategic Investments or as some observers put it, “Juncker’s new narrative regarding the importance of investment”75 – the focus was on a European investment offensive with stimulating financial incentives. The efforts to close the Europe-wide crisis-related investment gap without having to make excessive use of the EU budget were aimed at economic recovery, the creation of new jobs, and the development of European competitiveness.

At the heart of this offensive was the EFSI, a joint and coordinated initiative of the European Commission and the EIB to mobilise private investment capital for strategic investment projects in the EU. However, it is not a fund at all, but an initial Union financial guarantee of €21 billion: €16 billion from the EU budget and another €5 billion from the EIB. The term of this loan guarantee was initially limited to three years. Thanks to these guarantees, the EIB expanded its business volume by around €61 billion, which in turn – including private capital – should result in a total investment volume of at least €315 billion in the real economy over the three years. At the end of 2017, the Commission and the EIB extended their guarantees in the course of a first interim evaluation and adjustment. A total investment volume of €500 billion has now been targeted. The duration of the EFSI was extended until the end of 2020 and new funding targets were added.

In its evaluation report on the relevance, effectiveness, and efficiency of the EFSI, the EIB came to an overall positive conclusion. The EFSI had succeeded in “mobilising a large volume of investment”76 and achieving the set of investment objectives. The Commission was also very satisfied. According to the Commission, by October 2019 the EFSI had mobilised additional investments of €439.4 billion, increased the EU’s gross domestic product by 0.9 per cent, and created 1.1 million additional jobs. In addition, the EFSI’s impact would be felt in the long term, up until 2037.77 The European Court of Auditors, however, drew a mixed conclusion in its report. The EFSI had proved to be an “effective instrument”, even if the estimates of the mobilised investments were partly exaggerated and excessive. However, it has replaced funding from other EU financial instruments and overlapped with the European Structural Funds.78

But however one evaluates the work of the EFSI, the necessary close cooperation between the European Commission and the EIB has led to an expansion of the range of economic policy instruments in the hands of the Commission. “In this process, the European Commission has gradually expanded discretion over investment vehicles, including the EIB.”79 With the continuation of the EFSI in the new InvestEU Fund80 for the period 2021 to 2027, as proposed by the Commission, this trend towards a European investment management and steering policy, influenced primarily by the European Commission, could be continued and intensified.

The European Economy, the Green Deal, and the Pandemic

With the European Green Deal, the Commission, under its new president, Ursula von der Leyen, has proposed the next 10-year economic policy strategy. According to the European Commission, the Green Deal is a “new start”81 for European economic policy; the Union has “a unique opportunity” in the next decade “to lead the transition to a fair, climate-neutral and digital Europe”.82 With this strategy, the Commission wants to develop a European leitmotif that will in the future “put sustainability and the well-being of citizens at the centre of economic policy”.83 Economic growth is to be decoupled from the use of resources so that the “natural capital of the EU” can be protected and preserved, and this transition can be organised in a fair and inclusive manner. “Competitive sustainability” is “at the heart of Europe’s social market economy”.84

The transformation of the European economy in the long term is one goal of European economic policy-making; the other is to cushion the foreseeable deep recession as a result of the lockdowns to fight the Covid-19 pandemic.85 The EU institutions want to combine the short-term crisis response with massive economic stimulus and the long-term goal of a climate-neutral economy. Whether for the ambitious Green Deal or in response to the socio-economic consequences of the pandemic and the lockdowns, in both cases the EU is making use of its traditional instruments for European economic policy-making: regulation, competition and state aid law, economic policy coordination, and finally financial stimulus and incentives.

Internal market regulation and the scope for state aid and competition law

The internal market will remain at the heart of European economic policy. However, the Commission fears that “the further integration advances, the more politically challenging every ‘extra mile’ becomes as we touch on increasingly sensitive economic and social issues”. It therefore requires “more political courage and determination than 25 years ago, and greater effort than ever to close the gap between rhetoric and delivery”.86 The internal market needs to be developed, particularly in the areas of digital economy, capital, and financial markets and energy; services markets in particular offer the greatest potential for further integration.87 The development of new and sustainable digital technologies is a prerequisite to ensure the EU’s “technological sovereignty” and global leadership and to further stabilise the euro area with a banking and capital market union.88 The changes in worldwide economic structures and trade flows as a result of digitisation and globalisation will make adjustments of the European internal market – and thus of EU economic policy – inevitable.

The Commission has now presented an analysis89 of the main obstacles, 13 of them, to advancing integration in the internal market. With a total of 18 actions – ranging from new online platforms to the digitisation and modernisation of national administrations, as well as training and exchange of judges – the Commission90 aims to overcome these regulatory, administrative, and practical obstacles. The actions will be based on intensified cooperation and partnership between the monitoring and enforcement authorities in the member states and with the Commission, with the aim being to “enrich our lives in many ways” through “digital solutions such as communications systems, artificial intelligence or quantum technologies”.91 To this end, five years after an initial strategy92 for the digital internal market, the Commission has now presented a new data strategy93 and a White Paper on artificial intelligence.94

The Commission already tabled recommendations for the adaptation of existing European directives and regulations to the Green Deal, for example on the revision of the Emissions Trading System and its extension to additional sectors. By contrast, only a few truly new European legislative procedures were presented. What is new is the proposal for a European climate law,95 which will legally establish the common goal and the implementation path to climate neutrality by 2050. Also new are a CO2-limit compensation system and legal provisions to ensure a safe, cycle-oriented, and sustainable value chain for batteries. According to the European Commission, the Green Deal is intended to support the transition to climate-neutral production processes with adapted state aid regulations and guidelines, which, for example, offer financial support for companies that decarbonise or electrify their production processes. Member states should also be given greater financial leeway for the energy-efficient conversion of buildings and district heating networks, the transition to a circular economy, investments in energy production from renewable sources for own consumption, and aid to facilitate the phasing out of coal-fired power stations.

The economic shock caused by the Covid-19 pandemic has magnified the challenge. The resulting drastic slump in growth, the increase in unemployment, and business insolvencies in the EU also threaten the integrity of the internal market. To cushion the asymmetric consequences of the Europe-wide lockdowns for the economies united in the internal market, the EU member states agreed in April on an initial corona aid package of €500 billion. In addition to the provision of credit support to the euro countries through the European Stability Mechanism and the new €100 billion instrument SURE (Support to mitigate Unemployment Risks in an Emergency)96 to finance national short-time working schemes, the immediate measures focussed in particular on easing state aid control. The European Commission presented temporary state aid measures that it considered compatible with the single market and which it intended to approve very quickly following prior notification by member states. These included support measures such as direct grants, loans, guarantees, and tax benefits.97 By reviewing foreign investment, the Commission sought to protect strategic European companies and institutions. The Union responded to the supply shortages that became apparent at the beginning of the pandemic and to the disruption of global supply chains – an obvious market failure – with joint action on the procurement of medical products. Finally, to protect economic freedoms in the internal market, the Commission urged member states to keep their borders open for the exchange of goods and to allow the entry of workers, particularly in systemically important functions. Even in the crisis, the integrity and stability of the internal market thus remained at the forefront of European economic policy responses.

The new focus of the European Semester

With the European Green Deal, the Commission announced many new plans and strategies: a European climate pact; a strategy for sustainable finance; another called “From Farm to Fork” to improve the environmental performance of agriculture and food processing; a new biodiversity strategy; a strategy for sustainable and intelligent mobility; and an action plan for recycling. With the help of the European climate law, a legally binding target for achieving climate neutrality is to be agreed. The Commission intends to monitor and evaluate the national implementation and enforcement plans every five years. Should a member state deviate from the agreed European approach in its assessment, it can publish corresponding reform recommendations as part of the CSR in the framework of the European Semester.

In addition, thanks to the European Structural Funds, the priorities of public investment in the member states and the regions will be more closely coordinated across Europe and targeted towards the new climate policy objectives. Already for the European Semester 2019, the Commission had listed investment priorities for each member state in its annual country reports – and thus implicitly defined the priorities for support with Structural Funds – “in order to provide a clear roadmap for reforms”.98 In the future, member states will be required to incorporate the recommendations into their investment strategies and take them into account when implementing their structural support programmes. The investment guidelines thus identify the “priority investment areas and framework conditions for effective delivery of the 2021–2027 Cohesion Policy”.99 They also require member states to report regularly on their progress in implementing CSRs and their investment programmes.

The climate and sustainability goals of the Green Deal are becoming the guiding principle of the European Semester.

In the European Semester 2020, the Commission also integrated the 17 Sustainable Development Goals of the 2030 Agenda for Sustainable Development of the United Nations (UN).100 In the future, each country report will be accompanied by a statement on the state of implementation of these global goals in the respective member state.101 The European Semester, which was originally intended to promote economic growth and employment, will thus be expanded to include sustainability policy as well as environmental and social objectives – differentiated according to the specific circumstances of the member states, but closely coordinated at the European level.102

In this way, the technical and administrative coordination approach of the European Semester can be used for almost all policy areas. The Semester thus becomes the central steering instrument of a comprehensive European economic process policy. However, this extension of scope as well as monitoring capabilities is also being criticised: This, critics say, leads to an overburdening of the Semester, while the concentration on the original economic and financial policy reform goals and approaches is lost. Some member states fear there will be negative effects on the enforceability and binding nature of the instrument.

However, the Covid-19 pandemic has shown the need for closer economic policy coordination and the need to focus national strategies on common objectives and additional areas. The national crisis packages intended to contain the recession differ considerably regarding the financial volume being made available. However, the core aim of all programmes is to cushion the social and economic consequences of the crisis and to provide financial stimulus to revive the economies after the lockdowns. The measures now being taken at both the European and national levels to revive the economies are to be combined with the goal of climate neutrality. “Moving towards a more sustainable economic model, enabled by digital and clean technologies, can make Europe a transformational frontrunner,” says the European Commission.103

The EU is thus following the economic policy model of “green economic growth”, which has been in development since the turn of the millennium by international economic institutions such as the Organisation for Economic Co-operation and Development (OECD).104 In the course of a “holistic development strategy”, the CSRs on structural reforms and investment in the member states are to be adapted to the guideline of sustainable growth. Climate neutrality in the context of the Green Deal and the UN’s sustainability goals will thus become the guiding principles for economic recovery measures – at the regional, national, and EU levels – and for future European economic process policy.

Financial incentives to implement the Green Deal

In January 2020, the Commission presented a proposal to finance the calculated annual investment of €260 billion up to 2030 as a first specification of its Green Deal communication package. The money is to come from three sources: the EU and national budgets, the EIB, and the private sector.

In addition to its planning for the long-term European Green Deal and the immediate Covid-19 response, the Commission used the medium-term stimulus measures to further focus on its policy priorities. On 23 April 2020, the European Council, on the recommendation of ECOFIN, combined the approval of the first rescue package with a mandate to the European Commission to prepare a proposal for an additional recovery fund to provide strong economic stimulus. On 27 May 2020, the Commission presented this new proposal together with the European recovery fund “Next Generation EU” (NGEU) and linked it to its Green Deal and digitisation, that is, to its new growth strategy. The European Council endorsed this proposal in principle at its historically long, extraordinary summit on 17–21 July 2020. The aim now is to create a temporary cyclical budget alongside the usual seven-year financial framework. A total of €750 billion will be added to the European budget to provide targeted assistance to the regions and sectors most affected by the consequences of the pandemic.105

The Multiannual Financial Framework 2021–2027

The Commission’s original draft budget for the period 2021 to 2027, adopted in May 2020, already provided for 25 per cent of agricultural and Structural Funds to be invested in measures to achieve the common climate objectives.106 The European Council has now decided to further increase this amount to 30 per cent of the total European budget and also to focus the additional money from the temporary European Economic Recovery Plan, the NGEU, on climate action.

The temporary increase of €47.5 billion, the frontloading of European Structural Funds with the new programme ReactEU,107 and the newly created Just Transition Fund (JTF) for economic transformation support will mainly serve the EU’s two top economic policy objectives for the next decade – climate neutrality and digitisation. The new Recovery and Resilience Facility,108 totalling €672.5 billion (of which €312.5 billion will be in the form of non-repayable grants), will also support the Green Deal and digitisation priorities. As part of Europe’s response to the consequences of the pandemic, the Commission has therefore found a way to underpin the huge investment needs for the EU’s new green growth strategy with appropriately funded European support programmes.

The EIB as a motor for investment

The Commission has also presented and updated a new investment programme – the InvestEU Fund.109 Similar to the EFSI, it aims to secure private investment with the help of a guarantee from the EU budget. As part of the next Multiannual Financial Framework (MFF) and the NGEU, the Commission proposed a large EU budget guarantee of €31.6 billion for the InvestEU Fund. This should mobilise an investment volume of up to €400 billion. Sixty per cent of this money should be used from the “sustainable infrastructure window” funding area for climate policy objectives alone. The European Council drastically reduced the proposed amount and agreed guarantees of 2.8 billion in the MFF and 5.6 billion in the additional NGEU. Nevertheless, the revised EU investment programme will also serve the new growth strategy.

With InvestEU, the EFSI becomes the Commission’s permanent economic policy instrument.

The Juncker Commission’s initially temporary EFSI programme to revive the European economies after the euro crisis is thus being consolidated under a new name as an additional economic policy instrument of the Commission. As the national development banks are also to be directly involved in the new programme in the future, the InvestEU Fund will gain even more impact; at the same time, national investment decisions and support will be directed to European objectives.

The guarantee for private climate protection investments is also to be supplemented by the EIB’s transformation into the “Climate Bank of the EU” and by support programmes of the national development banks. The EIB is to gradually increase the share of its financing focussed on climate protection and environmental sustainability to 50 per cent of its financing volume by the end of the decade. The Commission hopes that this will result in a total investment of around €600 billion for climate protection.

The Just Transition Fund

In addition to these incentives and investments, the Commission proposes a Just Transition Mechanism to encourage the phasing out of fossil fuels (coal, peat, and shale gas) and to dampen the costs for the regions and sectors concerned.110 This mechanism will also consist of three elements: the new JTF mentioned above, a special transitional arrangement under the InvestEU Fund, and a new EIB public-sector lending facility.

What is really new is the proposal for an additional fund, the JTF. For this fund, the Commission had already presented a proposal for a regulation in January 2020,111 including the expected distribution of the funds among the member states.112 A revised version followed in May 2020,113 in which the originally estimated €7.5 billion was increased to around €10 billion and supplemented by an additional €30 billion from the temporary economic stimulus budget NGEU. The agreement of the European Council on 21 July 2020 now provides for significant cuts in this proposal. The heads of state and government agreed to set for the JTF in the next MFF a volume of €7.5 billion, and in the NGEU an additional €10 billion, bringing the total JTF budget to €17.5 billion. Member states will also have to complement the JTF allocations with reallocations from other European Structural Funds – the European Regional Development Fund and the European Social Fund – and national co-financing. Support will be provided for investment in SMEs; business start-ups and incubators; research and innovation; recycling; the use of new and clean technologies; digitisation; site restoration and decontamination; further training, retraining, and job search; and the active inclusion of job seekers.

The future role of the Commission

With its new growth strategy, the revised proposal for the next MFF, and the temporary cyclical budget NGEU, the Commission seems to be trying to strengthen its role in economic policy coordination and the European Semester. It is increasingly determining the priorities and focal points of European economic policy-making and the sequence of corresponding reforms in the member states; it monitors their implementation and compliance with European obligations; and it decides on flexibility or decisiveness in the assessments, and thus on the sanctioning or approval of member state policies.

European climate law creates the legal basis for more narrowly defined steering and European monitoring of national economic policy-making with regard to green and sustainable growth, in line with the objectives of the European Green Deal. The European Semester is developing into the key steering instrument of this green economic process policy: Its scope of application is being expanded, the instrument is being more closely interlinked with the EU budget, and it is thus becoming more effective. In the future, the allocation of European funding will be linked even more directly to the objectives, content, and recommendations of economic policy coordination; this will increase the efficiency of European Community economic policy-making. The objectives and guidelines for the European Semester and the country-specific reform recommendations, which will be supported by European funding, will in turn be based on the growth strategy of the Green Deal.

The Commission is becoming the dominant and guiding actor in European economic policy-making.

The permanent successor to the EFSI, the InvestEU Fund, will be managed by the Commission itself, with the EIB serving as its “preferred implementing partner”. At the same time, the Commission wants to work with national development banks and international financial institutions. With the introduction of investment guidelines in the European Semester and the targeting of corresponding support measures with the help of the Structural Funds, the Commission now has the possibility to co-determine national and regional investment priorities along the common European guidelines. The new JTF, which is to cushion the transition to climate-neutral growth, also serves the overarching economic policy objectives of the EU.