Michał Romanowski

WARSAW: The offensive US trade policy as well as economic sanctions Washington imposes on its adversaries have triggered a shift in the global currency landscape – and, as a result, steady recession from the dollar-denominated system. Called “de-dollarization,” this phenomenon fits into the wider narrative of a multipolar world of which a monetary order would be an integral component. Countries like Russia and China, given their international heft – ranked as second and twelfth leading economies, respectively – lead this process. Others including Iran, Turkey and major European countries are not lagging far behind.

WARSAW: The offensive US trade policy as well as economic sanctions Washington imposes on its adversaries have triggered a shift in the global currency landscape – and, as a result, steady recession from the dollar-denominated system. Called “de-dollarization,” this phenomenon fits into the wider narrative of a multipolar world of which a monetary order would be an integral component. Countries like Russia and China, given their international heft – ranked as second and twelfth leading economies, respectively – lead this process. Others including Iran, Turkey and major European countries are not lagging far behind.

Transition from the US dollar-based environment is possible, but will be slow and the new reality will involve a competition from several pretenders for the status of the dominant currency.

The US dollar is king and has enjoyed such global status for decades. When Saudi Arabia and the United States reached a deal in the 1970s to trade oil and therefore other relevant goods, only in US dollars, the role of the greenback was cemented. Today, over 60 percent of the world’s foreign exchange reserves are held in US dollars, and the greenback accounts for 70 percent of global trade transactions. Consequently, when virtually the entire globe uses the dollar to settle payments this generates major demand for the currency itself. The status allows the US government to refinance its debt at low interest rates through bonds and securities.

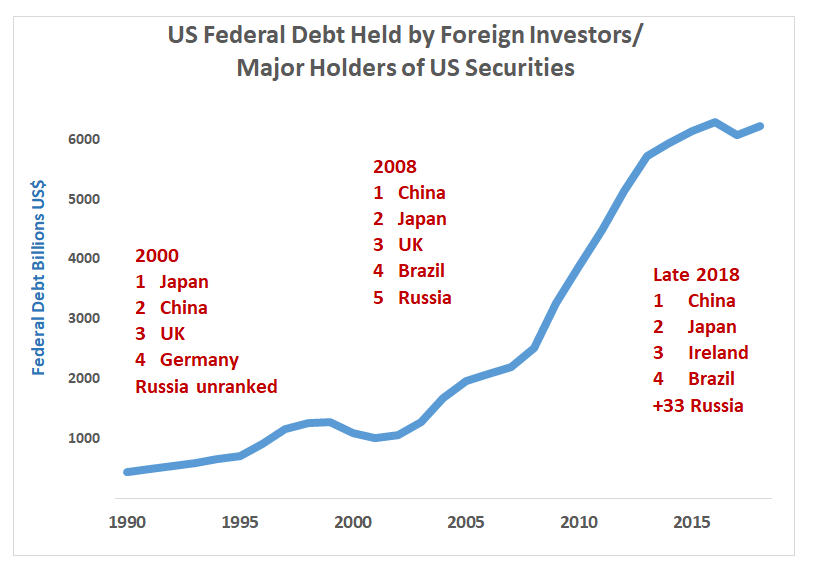

Lender snapshots: US debt has steadily risen in recent years; to influence dollar’s dominance, Russia needs China’s help (Source: US Federal Reserve and US Treasury Department)

Lender snapshots: US debt has steadily risen in recent years; to influence dollar’s dominance, Russia needs China’s help (Source: US Federal Reserve and US Treasury Department)

Global trade is not the only factor. With the growing economic posture of China, India and others, the transparency of the US financial system and monetary policy also make the dollar a safe-haven in a time of uncertainty or crisis. In fact, the greenback appreciates disproportional profits considering the size of the US economy, which is slowly but surely giving place on the international scene to rising Asian actors.

Countries around the world pursue de-dollarization not only due to US sanctions and trade wars. The large share of the greenback in the economy adversely affects the efficiency of states’ monetary policy and reduces capacity to control macroeconomic processes. When governments, banks or citizens hold sizeable dollar-denominated assets and liabilities, this trend can lead to significant income losses when exchange rates fluctuate.

Economists suggest that the challenges posed by high dollarization can be tackled only in a comprehensive manner. This requires not only ensuring price stability and exchange-rate flexibility, but also spurring a structural shift of the economy. Above all, trust in any national currency must be restored or instilled to produce positive results.

International Monetary Fund studies offer evidence that monetary and macro-prudential policies coupled with the introduction of inflation-targeting regime substantially de-dollarized emerging market economies in Latin America, Europe and Asia between 2000 and 2008. The trend has either stalled or partly reversed with the global economic crises, 2009 to 2011, but today returns in full force.

Russia, with more than its state budget relying on oil revenues, drives the de-dollarization train with President Vladimir Putin calling on the global dollar monopoly to end. Moscow hopes to enjoy the unlimited sovereignty and shield itself from US sanctions and external political pressure. Russian authorities are currently working on a de-dollarization plan that would stimulate payments in other currencies as well as transfer country’s major holdings to the Russian jurisdiction.

This year Moscow has already offloaded more than $80 billion in US government debt obligations, which equals 84 percent of its US securities. This exodus demonstrates that Russia is serious to move beyond political rhetoric and be a proactive player.

As the largest exporter of gas and the second largest of oil in the world, Russia has the theoretic claim to challenge the petrodollar. However, it can achieve no satisfactory outcomes alone.

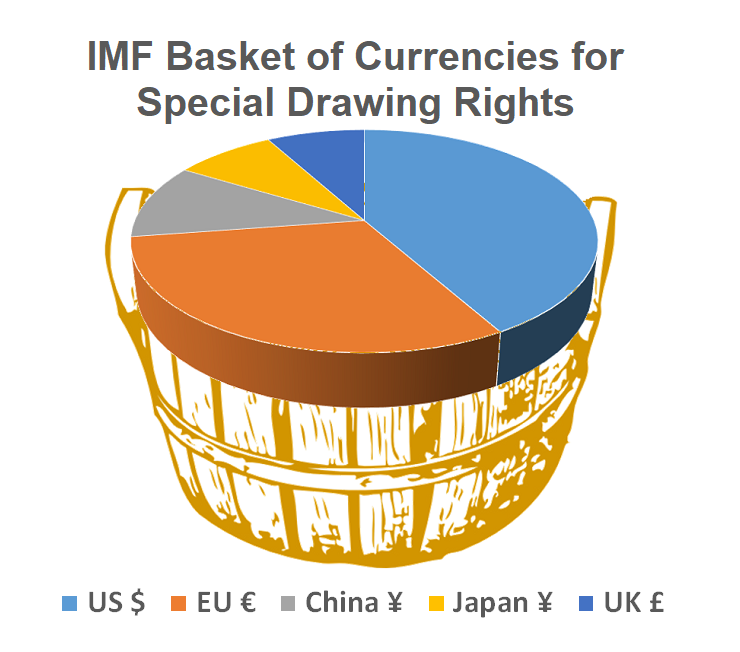

A changing basket: The International Monetary Fund reviews reserve currencies every five years and added the Chinese renminbi/yuan in 2015; criterion require that currencies are freely usable and widely traded (Source: IMF)

A changing basket: The International Monetary Fund reviews reserve currencies every five years and added the Chinese renminbi/yuan in 2015; criterion require that currencies are freely usable and widely traded (Source: IMF)

Enter China. Over the past years, Beijing has made significant progress in enhancing the yuan’s role in international trade and investment. The governor of China’s central bank criticized the globe’s dependence on the dollar in 2009, and almost a decade later, during the 2017 Congress of the Chinese Communist Party, President Xi Jinping said that the time has come for China to take center stage in the world. This includes not only promoting globalization and boosting foreign aid, but also internationalizing its currency.

Beijing is rather conservative about dumping shares of its $1.17 trillion holdings of US debt amid trade tensions with the United States. But leaders have already taken several essential steps to make the yuan a global currency. IMF awarded the yuan status as a reserve currency in 2015, adding it a year later to the Special Drawing Rights – a supplementary foreign-exchange reserve asset. In 2017 China overcame the United States to become the world’s largest importer of crude oil, and in March 2018, China launched first crude oil futures contracts priced in yuan – an open challenge to a petrodollar order.

Policymakers in Beijing have increasingly wondered why they should we pay for oil in dollars and not Chinese currency. This led to extending local currency swaps with various countries. China has already eliminated transactions denominated in US dollars from the bilateral trade with Iran and signed similar agreements with Canada and Qatar. But there are obstacles to China’s currency spread as well. The country’s capitals markets are underdeveloped and not fully accessible while yuan is not allowed to float freely as the government determines the rate. Also Beijing initiates its climb up the international currency ladder from a low point. SWIFT data indicate that the yuan accounts for approximately 2 percent of cross-border payments in comparison to a 40 percent share of dollar-denominated transactions.

Europe, for its part, watches these developments closely, but also takes action. In September 2018, President of the European Commission Jean-Claude Juncker said that Europe should do more to promote the euro. He described as “absurd” the situation in which the European Union purchases 80 percent of its energy in dollars while the United States provides 2 percent of raw materials required by Europe. The European Central Bank recently exchanged €500 million worth of US dollar reserves into yuan securities. It reflects both China’s growing prominence in the global financial system as well as the state of transatlantic relations which have never been so strained. And when German Foreign Minister Heiko Maas calls for abandoning SWIFT, ending US dominance and establishing a new payments system independent of the United States one could almost expect tectonic changes in the global currency environment.

The de-dollarization process poses international economic ramifications. The greenback’s near-monopoly in the sphere of payments and reserves has been challenged and a more multipolar currency landscape is gradually being developed. However, political consequences of these processes may be far more profound. When Saudi Arabia decides to accept yuan for oil sold to China, the United States – already perceived as turning inward – will unintentionally make political room for Beijing in assuming a greater leadership role worldwide.

In the foreseeable future the dollar will remain the dominant source of trade and payments. Currency guru Barry Eichengreen suggests the currency could lose its high status within 10 years. He reminds that the 20th-century sterling-to-dollar switch on the global scale was rapid, and the yuan is an underdog that might surprise all.

Michał Romanowski is a Eurasia expert with The German Marshall Fund of the United States in Warsaw.

This article was posted November 5, 2018.

No comments:

Post a Comment