ON THE campaign trail, Imran Khan, Pakistan’s new prime minister, presented himself as the man to break the country’s addiction to hand-outs from the West. Whereas previous governments used to go begging to the IMF for funds, he said, his Pakistan Movement for Justice (PTI) would focus instead on recouping billions of dollars hidden from the taxman abroad. But after less than two months in office, Mr Khan reversed himself on October 8th. His finance minister announced that the government would, after all, be seeking a big loan from the IMF.

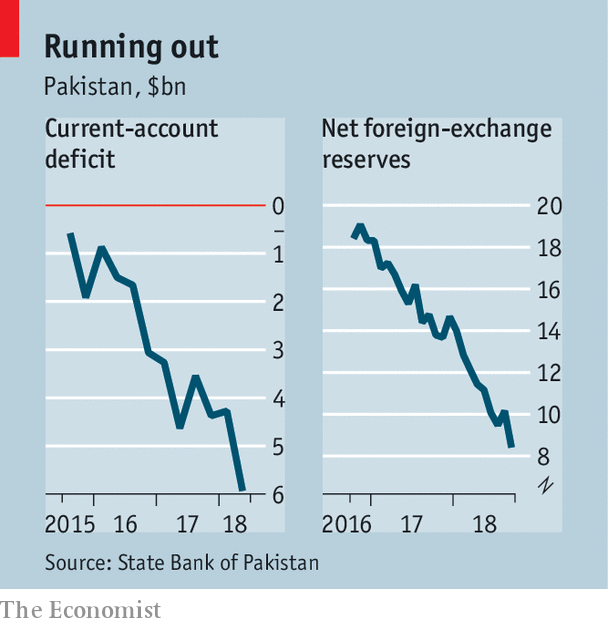

The economy’s troubles are not Mr Khan’s fault. The previous government, led by the Pakistan Muslim League-Nawaz (PML-N), lifted annual GDP growth to a ten-year high of more than 5%. But it did so on the back of expensive imports of fuel and machinery, even as its determination to prop up the Pakistani rupee hurt export industries such as textiles. The result has been dramatic growth in the current-account deficit since early 2016 (see left-hand chart). Foreign-exchange reserves have fallen sharply as a result (see right-hand chart). They currently stand at $8bn, which is not enough to cover the expected bill for imports and foreign-debt repayments until the end of the year. To keep the lights on (literally—many of Pakistan’s power plants run on imported coal), the government needs to find around $10bn in short order.

Get our daily newsletter

Even Mr Khan could see that Pakistan was going to need a loan. But for the past few weeks he has desperately been seeking alternatives to an IMF bail-out. In a televised address, he asked all Pakistanis living abroad to donate $1,000 apiece to the government, ostensibly to help pay for a big dam. To show that government funds would no longer be wasted, he has engaged in public displays of austerity. The government has auctioned off eight buffaloes kept to provide milk for the prime minister’s residence, along with 61 luxury cars.

As recently as October 7th Mr Khan held out hope that “friendly countries” would stump up loans, sparing him the embarrassment of turning to the IMF. Mr Khan has courted Saudi Arabia, in particular, visiting it on his first official trip abroad. Yet the Saudis did not offer a bail-out (it was “awful to beg”, sighed the commerce adviser, Abdul Razzak Dawood). Instead, they volunteered to invest in the China-Pakistan Economic Corridor (CPEC), a $60bn infrastructure scheme financed mainly by China. That seemed to upset China, Pakistan’s “iron brother”, oldest ally and another potential donor, so was dropped. Some observers had imagined that China might increase its lending to Pakistan rather than have the IMF pore over the details of the contracts behind CPEC, which have not been made public and are thought to be unfavourable to Pakistan. But even the prospect of a row over CPEC does not seem to have been enough to persuade China to become Pakistan’s lender of last resort.

As Mr Khan hunted for benefactors, investors panicked. The stockmarket had its biggest daily drop in a decade on October 8th, doubtless spurring the government’s reluctant reversal the same day. The delay, says Khurram Hussain, a journalist, has weakened Mr Khan’s hand in negotiations with the IMF over the terms of any loan. In addition to demanding a good look at CPEC contracts to make sure Pakistan can afford them, the fund is likely to push for further devaluation of the rupee, increased tax collection and higher interest rates. None of these readily aligns with Mr Khan’s promise to create an “Islamic welfare state”. But if Mr Khan was unsure of it before he assumed power, he must surely now realise that Pakistan’s problems run deeper than corrupt leadership. And if voters were unsure of it before they cast their ballots, they are quickly discovering that Mr Khan, for all his self-assurance and star power, cannot fix things quite as quickly or easily as he promised.This article appeared in the Asia section of the print edition under the headline "Imran can’t"

No comments:

Post a Comment