China’s dying labour-force boom, like the Soviet Union’s in the 1970s, may not revive even with Silk Road project’s heavy investments.

China’s dying labour-force boom, like the Soviet Union’s in the 1970s, may not revive even with Silk Road project’s heavy investments.

What causes empires to fall?

According to one influential view, it’s ultimately a question of investment. Great powers are the nations that best harness their economic potential to build up military strength. When they become over-extended, the splurge of spending to sustain a strategic edge leaves more productive parts of the economy starved of capital, leading to inevitable decline. That should be a worrying prospect for China, a would-be great power whose current phase of growth is associated with an increasingly aggressive military posture and a tsunami of capital spending in its strategic neighborhood.

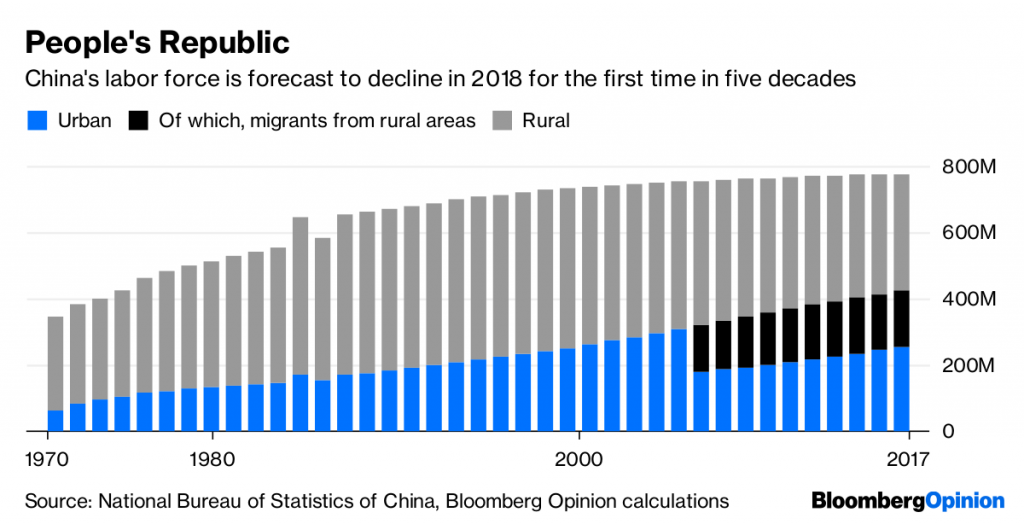

Like the Soviet Union in the 1970s, China is coming to the end of a long labour-force boom, and hoping that an orgy of investment will keep the old magic going while stabilising its fraying frontiers. The success or failure of its Belt and Road projects – and the still greater sums it’s spending domestically – will determine whether the nation achieves its dream of prosperity or succumbs to the same forces that doomed the USSR. China’s labour force might decline for the first time in five decades in 2018 | Bloomberg via National Bureau of Statistics of China

China’s labour force might decline for the first time in five decades in 2018 | Bloomberg via National Bureau of Statistics of China

China’s labour force might decline for the first time in five decades in 2018 | Bloomberg via National Bureau of Statistics of China

China’s labour force might decline for the first time in five decades in 2018 | Bloomberg via National Bureau of Statistics of China

The conventional worry about the Belt and Road initiative – an open-ended framework for an estimated $1.5 trillion of infrastructure projects over the next decade across Southeast Asia, South Asia and Central Asia – is that it will doom the recipients of its largess to a future as indebted clients of Beijing.

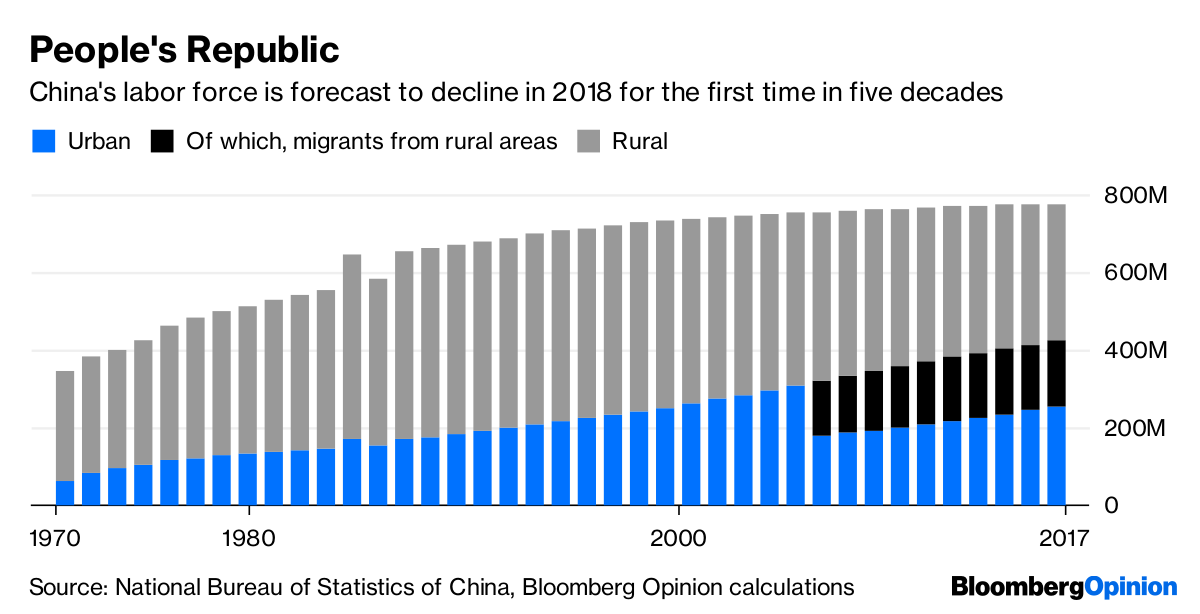

Failed projects like Sri Lanka’s Hambantota port may indeed be a way for China to quietly extend its strategic power around the world. But defaults on investments cause problems for creditors as well as debtors. The risk for president Xi Jinping is that the toll of all that misdirected spending gradually undermines the productivity growth on which China’s current might was built. Belt and Road Initiative’s projects in South Asian countries | Bloomberg Opinion

Belt and Road Initiative’s projects in South Asian countries | Bloomberg Opinion

Belt and Road Initiative’s projects in South Asian countries | Bloomberg Opinion

Belt and Road Initiative’s projects in South Asian countries | Bloomberg Opinion

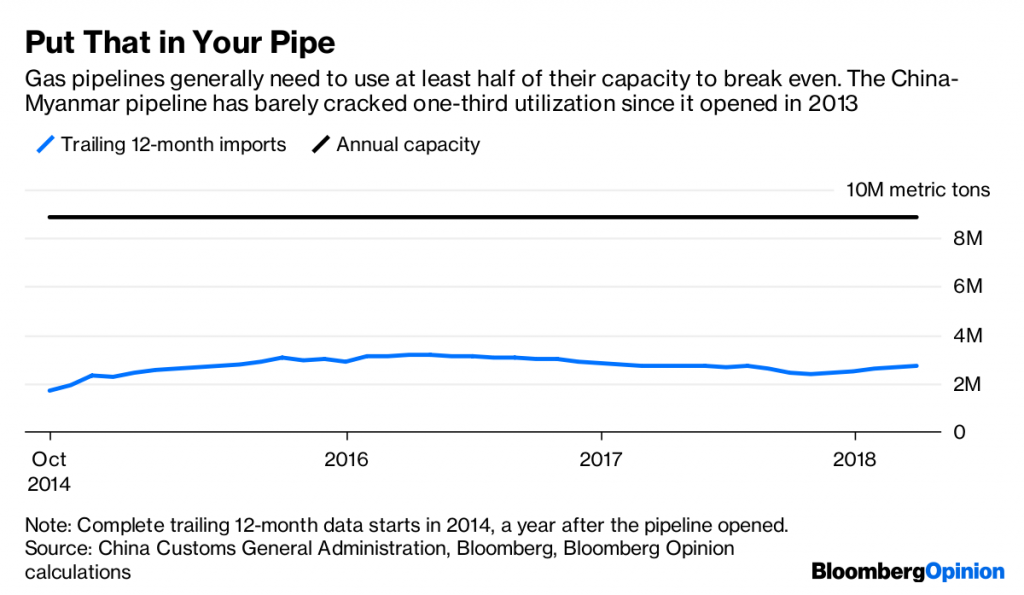

Consider some of the projects still on the drawing board. Think the $1.6 billion price tag Nomura Holdings Inc. has put on Hambantota looks excessive? Then check out Kyaukpyu in Myanmar, where Citic Group Corp. is leading the construction of a $9.6 billion deep-sea port and industrial zone to hook up with oil and gas pipelines built by China National Petroleum Corp. China-Myanmar pipeline’s unsatisfactory output | Bloomberg via China Customs General Administration

China-Myanmar pipeline’s unsatisfactory output | Bloomberg via China Customs General Administration

China-Myanmar pipeline’s unsatisfactory output | Bloomberg via China Customs General Administration

China-Myanmar pipeline’s unsatisfactory output | Bloomberg via China Customs General Administration

There’s certainly a strategic logic here. China’s links to the western markets that consume its goods and the Middle Eastern countries it depends on for petroleum pass through a choke point in the straits of Singapore and Malacca, a worry for the country’s military planners. Building railways and pipelines to the Indian Ocean provides an alternative route west.

On the economics, however, the idea falls down. The gas pipeline to Kyaukpyu has barely run at one-third of capacity since it was inaugurated in 2013, and the parallel oil tube sat dry for years before the first cargo was loaded up last year – not a great return on the $2.5 billion spent building them. A 260,000 barrels-a-day processing plant at the end of the pipe in Kunming that’s about the size of the UK’s biggest oil refinery will be similarly underutilised unless more crude deliveries arrive at Kyaukpyu.

Or take the web of touted rail projects through central Asia which form a centerpiece of most maps of Belt and Road projects. As we’ve argued before, such plans misunderstand both the long history and basic economics of east-west trade, which has almost always been far more dependent on maritime transport via Southeast Asia, India and the Arabian Peninsula than on overland Silk Roads through the Eurasian steppe.

The disadvantages of land transport are compounded these days by the existence of giant container ships capable of carrying almost $1 billion of cargo at a time, and the variety of different track gauges across Asia which require costly and time-consuming transfers.

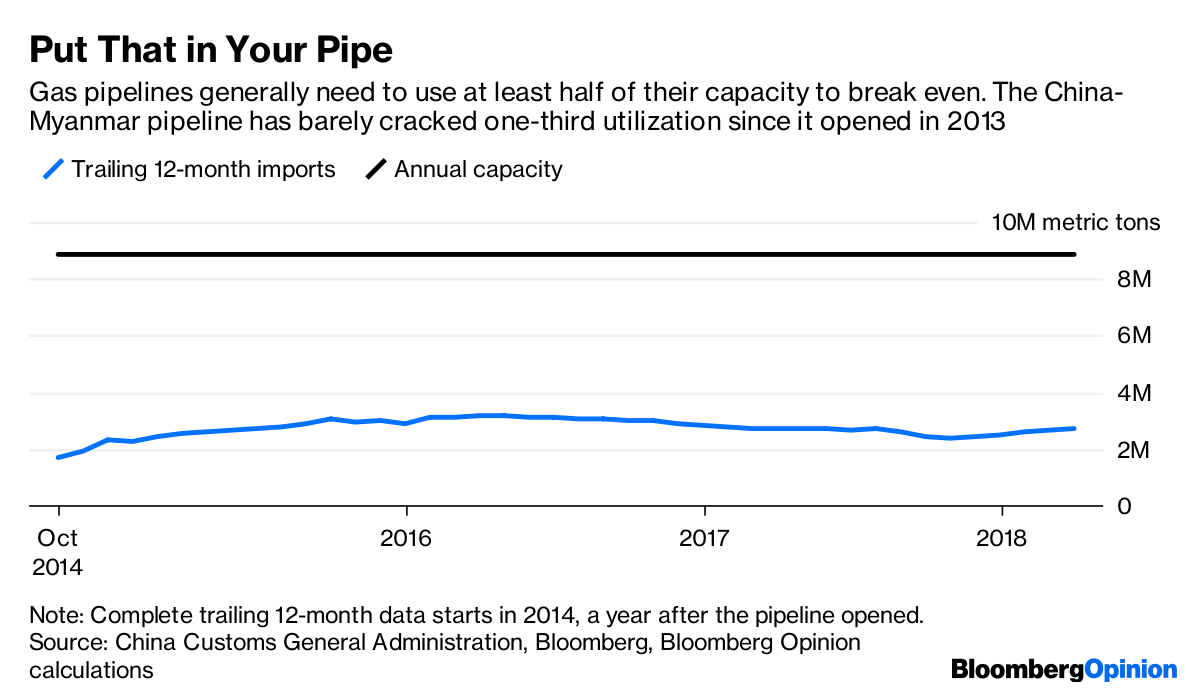

The value of freight between Europe and Yiwu, a much-touted overland rail hub near Shanghai, came to 2.27 billion yuan ($330 million) in the first four months of this year, according to China Railway Express Co. That’s about one third of what you’d get on a single mega-container ship, and there are hundreds of somewhat smaller vessels plying east-west routes. China’s top four ports alone process about the same value of cargo every three hours. China’s freight trade with Europe by sea, air and land | Bloomberg via Centre for Strategic and International Studies

China’s freight trade with Europe by sea, air and land | Bloomberg via Centre for Strategic and International Studies

China’s freight trade with Europe by sea, air and land | Bloomberg via Centre for Strategic and International Studies

China’s freight trade with Europe by sea, air and land | Bloomberg via Centre for Strategic and International Studies

It’s worth considering all this misdirected spending in the context of the Soviet Union’s decline. Around the middle decades of the 20th century, Moscow presided over a China-style economic miracle that caused many in the West to fear they would be overtaken. In the 1950s, the Soviet economy grew faster than that of any other major country barring Japan.

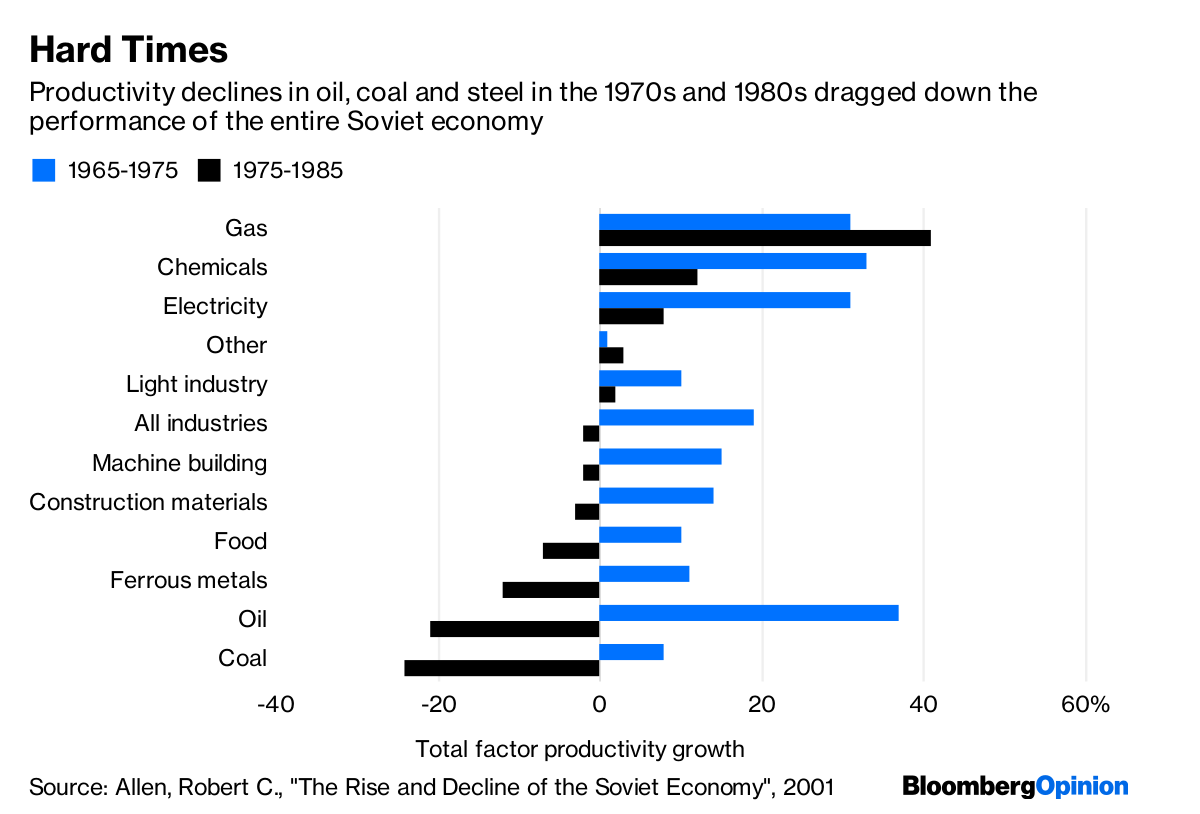

There are many reasons this development path started to falter in the 1970s, including the rigidities of a planned economy, a plateau in industrial workforce numbers, and the vast sums dedicated to Cold War-era military spending. Still, it’s hard to tell the story of declining Soviet productivity without also considering its own Belt and Road initiative, the development of Siberia.

From the 1960s, Siberia sucked up about a third of the Soviet Union’s heavy-construction equipment despite hosting just a fraction of the country’s population, as Moscow pumped in capital to develop gas fields, coal mines, aluminum plants, and a duplicate of the Trans-Siberian railway several hundred kilometers to the north.

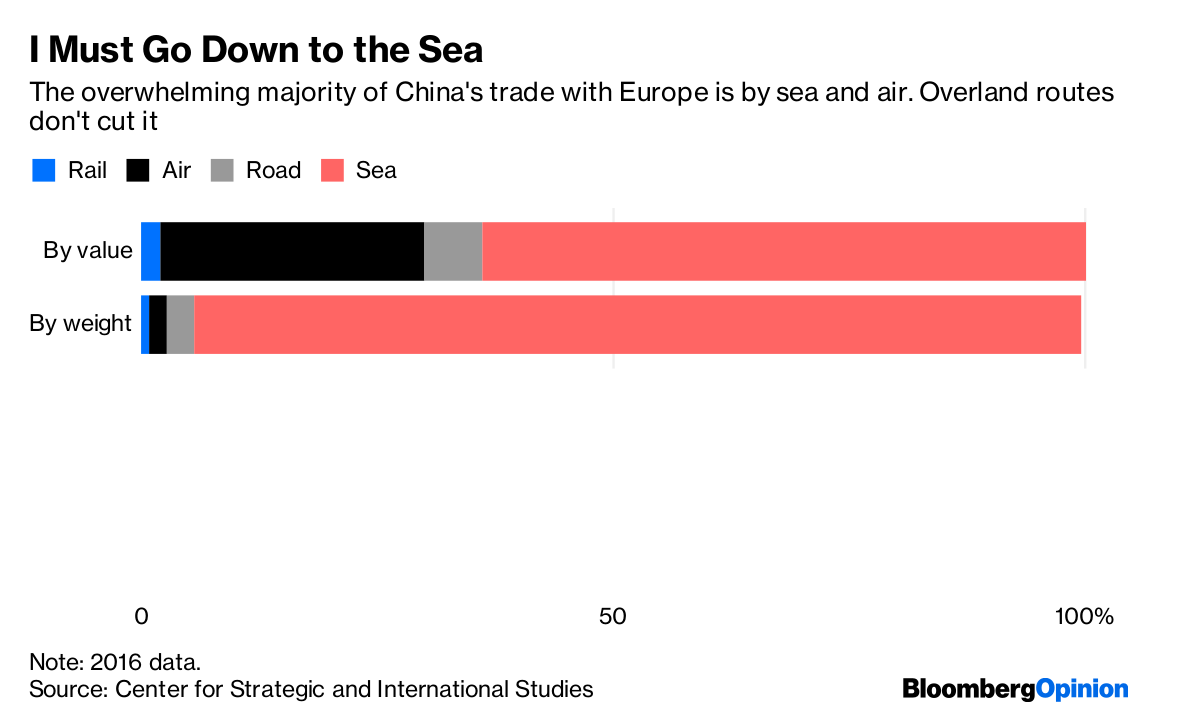

“The development of Siberian natural resources was a vast sink for investment rubles,” as economist Robert C. Allen wrote in a 2001 paper, diverting spending from more attractive projects west of the Urals and eventually undermining the productivity of the economy as a whole. “The Soviet Union’s ‘abundant’ natural resources had become a curse,” he wrote. “Resource development swallowed up a large fraction of the investment budget for little increase in GDP.” Soviet economy during the Cold War era | Bloomberg via Allen, Robert C, “The Rise and Decline of the Soviet Economy”, 2001

Soviet economy during the Cold War era | Bloomberg via Allen, Robert C, “The Rise and Decline of the Soviet Economy”, 2001

Soviet economy during the Cold War era | Bloomberg via Allen, Robert C, “The Rise and Decline of the Soviet Economy”, 2001

Soviet economy during the Cold War era | Bloomberg via Allen, Robert C, “The Rise and Decline of the Soviet Economy”, 2001

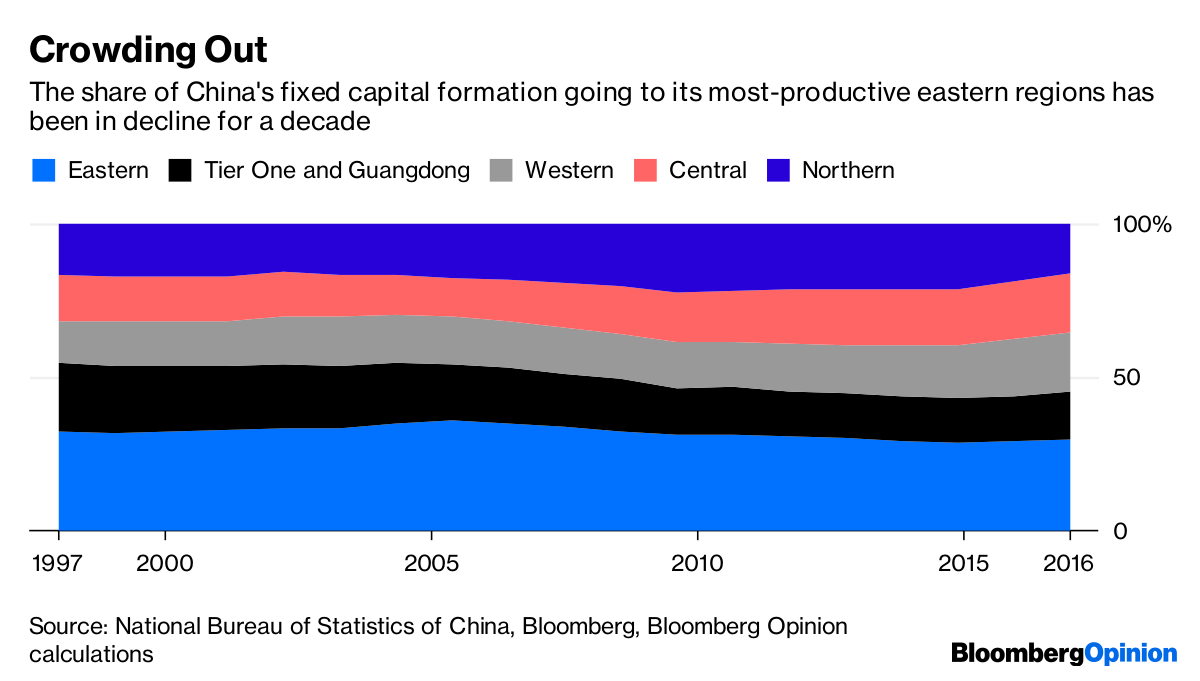

Could something similar happen in China? As with the USSR’s strategic concerns about shoring up its eastern fringes, Beijing’s fears of separatism in its west have driven a surge in capital projects there in recent years, next to which Belt and Road projects look like merely the tip of the iceberg.

Western China accounted for about 19.5 per cent of the country’s fixed capital formation in 2016, compared to 15.4 per cent in its dynamic Tier One cities and Guangdong province. Less developed parts of central, northern and western China have swallowed up the bulk of fixed capital ever since 2007, according to official data. China’s fixed capital formation over the past two decades | Bloomberg via National Bureau of Statistics of China

China’s fixed capital formation over the past two decades | Bloomberg via National Bureau of Statistics of China

China’s fixed capital formation over the past two decades | Bloomberg via National Bureau of Statistics of China

China’s fixed capital formation over the past two decades | Bloomberg via National Bureau of Statistics of China

That’s matched the end of China’s productivity miracle, too. Unit labour costs have outpaced productivity growth since 2008, meaning the economy has been growing less and less competitive over time, according to a report last month by the Conference Board, a research group. About 90 per cent of China’s advantage over the US in terms of unit labour costs in 2016 was explained by currency effects alone, economist Siqi Zhou wrote.

China’s anxiety about its western fringes has many troubling effects. Compared with the hundreds of thousands of Uighurs who’ve been sent to re-education camps and the millions more under constant surveillance in Xinjiang province, wasted capital on transport mega-projects may seem like a minor problem.

It’s not, though. In a country where reliable economic data is thin on the ground and the number of people in work is now in absolute decline, the toll of ill-conceived investments risks eating away at the foundations of growth.

China’s rise this century was driven by its embrace of world trade and the coastal provinces most exposed to it. In this retreat inland, it’s sowing the seeds of decline. – Bloomberg

No comments:

Post a Comment