According to John Forrer, economic sanctions can be considered ‘well-aligned’ when they inflict a specific amount of economic damage on a targeted individual or group within a limited time frame. The author acknowledges the difficulties in enacting such precise measures, but contends that the process might be made easier if states would 1) further develop analytic tools and techniques; 2) construct flexible economic sanctions able to adapt to changing circumstances; and 3) create a multilateral forum for data sharing and collaboration between states.

According to John Forrer, economic sanctions can be considered ‘well-aligned’ when they inflict a specific amount of economic damage on a targeted individual or group within a limited time frame. The author acknowledges the difficulties in enacting such precise measures, but contends that the process might be made easier if states would 1) further develop analytic tools and techniques; 2) construct flexible economic sanctions able to adapt to changing circumstances; and 3) create a multilateral forum for data sharing and collaboration between states.

Under the leadership of Andrea Montanino, director of the Atlantic Council’s Global Business & Economics Program, and Ambassador Daniel Fried, distinguished fellow at the Atlantic Council and former coordinator for sanctions policy at the US State Department, the Economic Sanctions Initiative is building a platform for dialogue between the public and the private sector to investigate how to improve the design and implementation of economic sanctions. To forge a path toward more effective economic sanctions, the initiative has a focus that goes beyond a purely national security perspective on sanctions to bridge the gap with the broader business perspective.

Well-aligned economic sanctions inflict a prescribed amount of economic loss, for the necessary period of time and affecting specific constituencies in the sanctioned country, sufficient to achieve the identified foreign policy goal(s), with the least amount of unwanted harm on other constituencies.

Designing and implementing economic sanctions that meet these criteria is an important foreign policy objective for several reasons. First, the sanctions are more likely to accomplish the desired foreign policy goal(s) they are meant to achieve. Second, they can be used as a credible tool of deterrence when threatened in advance of adoption, potentially gaining the benefits of economic sanctions without actually invoking them. Third, they strengthen multilateral cooperation, further increasing prospects for attaining the sought-after foreign policy goal(s). Fourth, they limit suffering of innocents living within the sanctioned country. Fifth, they minimize losses to businesses and consumers in the sanctioning country and those of its allies.

Poorly aligned economic sanctions will not only be ineffective, at times they may be a “cure that is worse than the disease.” Economic sanctions that prove to possess limited powers of persuasion may be categorized as symbolic, but they still cause real and unnecessary losses on individuals, firms, and communities to no purposeful end. In addition, they create a false impression of having taken meaningful action against another country’s policies. Failed efforts to bring about any change can also prompt an imprudent escalation of confrontation, as the sanctioning country may want to demonstrate its resolve, and that of its political leaders. Poorly aligned sanctions can be adjusted after the fact, potentially strengthening their potency, but the aim always should be to design well-aligned economic sanctions at the outset.

Challenges to Aligning Economic Sanctions

Achieving an alignment of economic sanctions presents numerous challenges. Historical studies of economic sanctions have identified only a handful of examples where sanctions were well-aligned enough to unambiguously achieve their intended goals.1 The effectiveness of many economic sanctions currently in place—against the Russian Federation for annexing Crimea, North Korea and Iran for their nuclear weapons programs, and Venezuela for subverting democratic institutions—is very much in question. Are they having the intended economic consequences? Are they forceful enough? Are the political leaders in the sanctioned countries suffering lost popularity as a result? How much longer do they need to be in place before they achieve their goals?

Aligning economic sanctions calls for imposing a level of sustained economic loss sufficient to achieve a change in the sanctioned country’s policies. And yet, estimates of how much economic suffering must be accomplished in quantifiable terms (e.g., lost gross domestic product [GDP], lost revenue from banned trade, or lost foreign direct investment [FDI]) for any given sanctions regime are rarely articulated. Such estimates are missing from public policy debates over the merits of existing or proposed economic sanctions. For example, what level of economic losses would Russia need to suffer and for how long for President Vladimir Putin to reverse the annexation of Crimea?2 When individuals or organizations are the targets of sanctions, the sanctioning country identifies specific constituencies in the sanctioned country who might respond to economic losses, but will freezing financial assets located in the sanctioning country be enough to persuade the targeted entities and individuals to change their behavior?

Aligning economic sanctions requires accurate and timely information on not only the sanctioned country’s economy, but also on its commercial and financial relationships with other countries—both current and potential. If current exports are sanctioned, what other markets are available for those same exports? How quickly can the sanctioned country establish new trading partners? How much more costly are these new transactions than pre-sanction trades? If access to financing from banks is sanctioned, what other institutions or governments might provide loans? Who else might invest in the sanctioned country? What are the prospects for avoiding sanctions restrictions and making unreported financial dealings?

The recent US expansion of sanctions against Venezuela to target that country’s public officials, including President Nicolás Maduro, has been accompanied by discussions on banning all US imports of Venezuelan crude oil. The United States is a major importer of petroleum from Venezuela and Venezuela’s economic health relies heavily on crude oil exports. But US economic sanctions banning petroleum from Venezuela could be less effective than expected. Venezuelan crude exports could be redirected to China, India, or the European Union (EU), as global petroleum markets adjust to the United States shifting its crude oil imports away from Venezuela to other countries. Rather than denying Venezuela the revenues it now receives from exports to the United States, a US ban on Venezuelan crude oil would force the rerouting of current global petroleum trade flows—no doubt at some loss to Venezuela due to higher transportation costs but not a crippling blow to its economy. Aligning economic sanctions requires an understanding of a country’s vulnerability to a specific set of sanctions as designed and implemented, but also an assessment of the extent to which the sanctioned country could take actions to avoid the sanctions’ sting. For example, economic sanctions on North Korea have been evaded by that country for years through smuggling, renaming companies, and falsifying cargo lists.

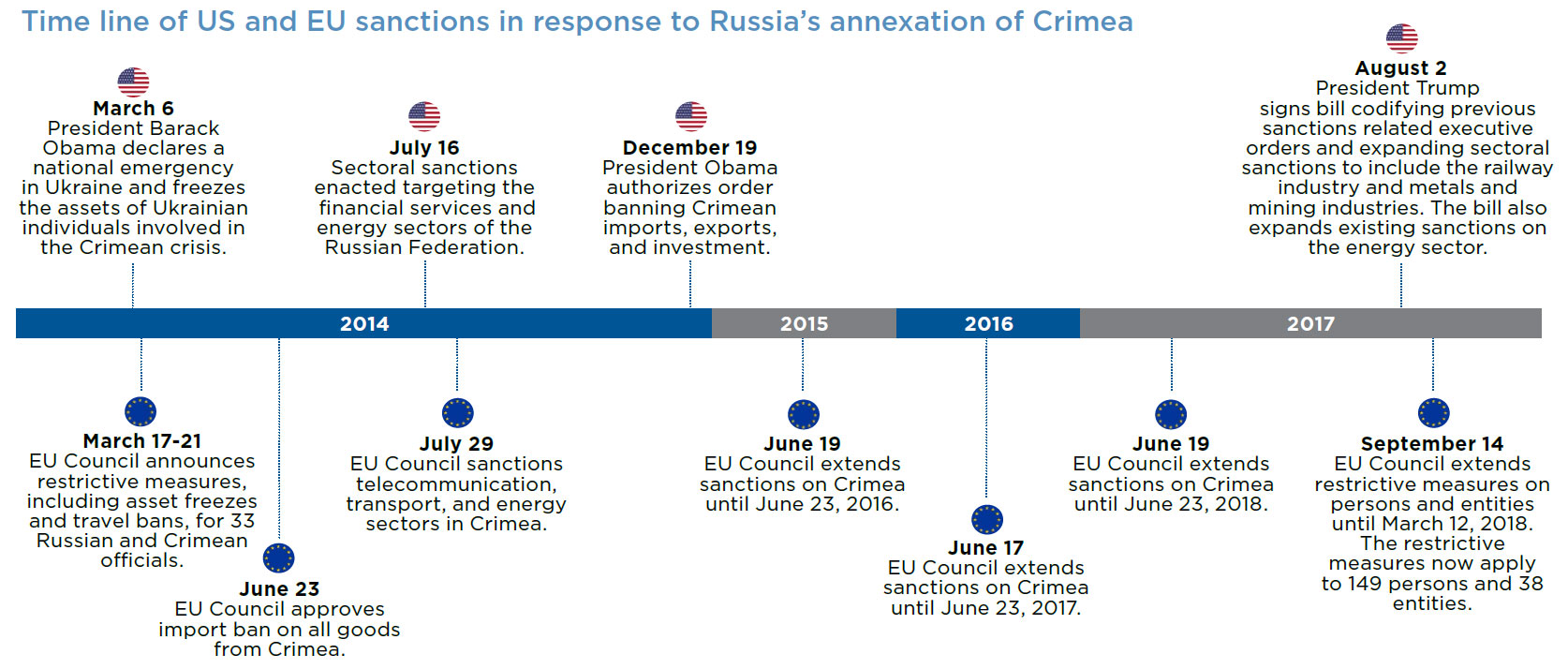

In addition, aligning economic sanctions requires making accurate predictions about future trends in the sanctioned country’s economic performance: How quickly is the economy growing? What are future prospects for FDI in targeted sectors? What are the trends for the value of its currency? How much debt does it owe already and what are the prospects for future lenders? For example, on March 17, 2014, the United States, the EU, and Canada introduced the first round of specifically targeted sanctions on Russia for its imminent annexation of Crimea. The sanctions restricted investments in the oil-producing sector and Russian banks’ access to foreign lenders and investors. The goal was to pressure Russia into a withdrawal from Crimea. A few months later, world crude prices began their precipitous fall from a peak of over $100 per barrel (bbl) to under $27 per bbl by February 2016. Today, world crude prices hover around $46 per bbl. The price drop has severely impacted the economies of petroleum-exporting countries. The economic losses caused by dramatically reduced world crude oil prices (and those of other related fuels) eclipse the potential impact economic sanctions would have had on the Russian economy on their own. While the sanctions on Russia affect sectors other than oil and gas, their net effect is now difficult to discern given the broader negative consequences of depressed crude oil prices.

From left to right, President of the European Commission Jean-Claude Juncker, President of the United States Donald Trump, and President of the European Council Donald Tusk. The three leaders pose for a photograph at the European Union headquarters in Brussels prior to bilateral discussions in May. Photo credit: Flickr.

Multilateral efforts pose their own challenges to aligning sanctions. As a rule, multilateral sanctions are considered to be more effective than unilateral sanctions. They expand the number of countries that inflict economic losses on the sanctioned country and decrease the sanctioned country’s options for evading the sanctions’ overall effects. However, attempts to align multilateral sanctions face an additional dimension of complexity. For example, Chinese firms and banks have continued their relationships with North Korea, justified by humanitarian concerns over the sanctions’ effects on North Korean citizens. The United Nations’ (UN’s) mandated ban on select North Korean exports and other commercial activities may be the “gut punch” as claimed by some,3 but slack enforcement of sanctions by trading partners important to the North Korean economy (e.g., China, Russia) will likely result in a much milder impact than the projected annual $1 billion in losses. The UN Security Council demonstrated its unity in calling for North Korea to end its nuclear and ballistic missile programs, but will the same united effort be shown when it comes to implementing the adopted sanctions? And if not, will the efforts of countries that do adopt the sanctions be wasted—the actual impact of their own sanctions on North Korea blunted by lax enforcement by others? Some participating nations might be willing to adopt even stricter sanctions than the multilateral sanctions approved by the UN if it were known that compliance efforts by some countries would be weak.

Stricter enforcement of a set of sanctions by the sanctioning countries is often held out as a way to make multilateral sanctions more effective, yet this strategy’s efficacy hinges on how well the sanctions are aligned in the first place. For example, as tensions have grown with North Korea due to its continued missile launch provocations, the Donald Trump administration has repeatedly singled out China as a lax enforcer of international sanctions on North Korea. New calls for China to tighten its enforcement of sanctions are coupled with threats of secondary sanctions against China if it fails to act. But if the economic sanctions against North Korea were not well-aligned to begin with, there are a number of consequences: there are no reliable projections of the level of economic losses needed to bring about a change in North Korea’s policies; there are no reliable estimates of the actual economic losses incurred by North Korea; and there are no reliable estimates of the suffering of innocents inside North Korea due to sanctions. What benefits arise from pressing for stricter enforcement of UN multilateral sanctions when their potential to be successful is largely undocumented?

Designing and implementing well-aligned economic sanctions is even more difficult in informal multilateral alliances. For example, both the United States and the EU adopted economic sanctions in response to Russia’s annexation of Crimea, but the two sanctions regimes differ in their terms and conditions. As a result, the two sets of sanctions regimes are both complementary and in conflict regarding their overall effects. The United States and the EU have different foreign policy interests in the conflict over Crimea, and adopting economic sanctions against Russia affects their own economies in different ways. Plus, it is impossible to predict whether any partner in a multilateral economic sanctions regime might adopt tougher sanctions or revoke existing sanctions in the future. Ideally, multilateral sanctions would be designed to consider all the options available to all potential sanctioning countries and select the portfolio of sanctions that optimizes alignment and offers the greatest chance for success. Of course, this is easier said than done.

Finally, inflicting the appropriate level of economic losses on constituencies in the sanctioned country with a minimum of unintended and residual economic costs is an important condition of well-aligned economic sanctions. However, predicting in advance the effect of sanctions on innocents in the sanctioned country is very difficult. Reliable data are often scarce. It is most common for anecdotal information to be presented after sanctions have been imposed, but there exist severe limitations on making accurate assessments on the sanctions’ impacts on specific groups within the sanctioned country or even the population in general, and even this information may not always be reliable. For example, economic sanctions imposed on Iraq after the first Gulf War were anticipated to affect the Iraqi people adversely. In 1995, the UN Food and Agriculture Organization reported that over 575,000 children had died related to the effects of economic sanctions.4 A UNICEF study later reaffirmed the finding,5 and it has been cited widely ever since as an authoritative figure. However, a new study is debunking the statistic as a “factoid.”6 The authors claim the original reports were based on falsified data provided by the Saddam Hussein regime. Their research shows that the economic sanctions in question had no discernable effect on Iraqi child mortality rates.7

Better-aligned economic sanctions make for more effective foreign policy tools. However, as described above, accomplishing such an alignment involves facing major challenges. Available data and analytics are insufficient for the task at hand: they are neither disaggregated nor robust enough; they are not available over long enough time periods; and they are sometimes simply unavailable. The world economy is dynamic and volatile: what is true today may have limited relevance for analyzing economic sanctions tomorrow. Too often, assessments of economic sanctions’ potential to achieve the desired foreign policy goal(s) are viewed exclusively through the lens of international affairs, with limited contribution of how their actual effects might be mediated by the realities of the global markets and the insights gained from employing a business perspective. Aligning economic sanctions requires better metrics and analytics, and a more comprehensive and holistic view that anticipates and accounts for their actual consequences on sanctioned and sanctioning countries, and others, in practice—not just in theory.

Credit: Michael Farquharson, Intern at the Atlantic Council’s Global Business & Economics Program

Aligning Economic Sanctions: The Case of Russia

A short description and assessment of the US and EU economic sanctions on Russia in response to the annexation of Crimea illustrates in detail the challenges of aligning economic sanctions.

The United States and the European Union have adopted three types of sanctions against Russia: targeted, sectoral, and comprehensive. Targeted sanctions apply to individuals with close ties to Russian President Vladimir Putin and those who have influence over powerful Russian institutions; these sanctions consist of visa bans and asset freezes.8 Targeted individuals include Yuri Kovalchuk, chairman of Bank Rossiya, and Igor Sechin, executive chairman of Rosneft, a large state-owned oil company.9

Sectoral sanctions have been applied to key industries of the Russian economy, notably finance, energy, and defense.10 They restrict Russian firms’ access to equipment, technology, capital, and technical expertise from the EU and the United States. For example, all three of Russia’s largest banks—Sberbank, VTB Bank, and Gazprombank—and energy giants Rosneft and Novatek have been denied access to loans with terms longer than thirty days.11

Comprehensive sanctions apply to the territory of Crimea, and prohibit all forms of commercial and financial transactions.12 US and EU citizens—no matter where they may be living—are prohibited from investing in Crimea, and neither individuals nor entities may import or export goods or services to or from Crimea.13

This author could not find any figures estimating the economic losses sanctions would need to inflict on Russia to bring about a change in its policy towards Crimea, or estimates of the extent to which the adopted sanctions impose those losses. Without such a baseline, comprehensively assessing how the current US and EU sanctions will impact Russia’s actions regarding Crimea is very difficult.

Quantifying with certainty the economic consequences of current sanctions on Russia is also challenging. The Russian economy relies heavily on revenue from exported petroleum products.14 The drop in revenue from reduced Russian crude oil exports, due to the sanctions, has caused significant strains on Russia’s economy. However, the severe worldwide drop in crude oil prices that quickly followed the adoption of sanctions on Russia clouds the assessment.15 A weaker demand for investment in Russian oil fields— due to lower oil prices globally—dilutes the effect the sanctions restrictions have on investors. No doubt economic sanctions have added to Russia’s economic distress, but if the cause of losses associated with economic sanctions cannot be distinguished from the losses due to depressed crude oil prices, the sanctions’ significance is shrouded and their efficacy undermined.

There is also some evidence that Russian firms are able to adapt to and, in some cases, circumvent the sanctions. Various loopholes—often centered on the re-exporting of banned products—have allowed a wide variety of goods to cross between the sanctioning countries and Russia. For example, Belarusian imports of EU cheese increased by 423 percent after the product was banned by Russian counter-sanctions, while Belarusian exports to Russia of the same goods grew simultaneously. Meanwhile, despite the sanctions and suspension of some partnerships with foreign corporations, Russian energy firms continue to explore the Arctic for oil deposits (enabled in part by limited European enforcement).16 Investors from Middle Eastern and Asian countries have expressed interest in helping to close whatever financing gaps have been caused by economic sanctions. Moreover, this author did not find any measures or estimates of collateral or unintended economic losses on people and businesses inside Russia or in the United States, EU, and their allies.

Finally, US and EU sanctions have had no discernable effects on Russian policy toward Crimea. Russia retains control over Crimea and continues to invest in the region, expanding efforts to build transportation linkages to Russia, while using the peninsula as an important military outpost for its Black Sea Fleet.17 And rather than undermining Putin’s status in Russia (as some may have hoped for), sanctions have more likely had the reverse effect by playing into his anti- Western rhetoric.18 From the US and EU perspective, the one tangible area of success has been in the realm of slowing military modernization. The weakening Russian economy and bans on Western exports of defense and dual-use technologies to Russia appear to have impeded the full implementation of much-needed updates and reforms.19

From left to right, Chief of the General Staff of the Armed Forces of Russia Valery Gerasimov, Russian Minister of Defence Sergei Shoigu, Russian President Vladimir Putin, Director of Russia’s Federal Security Service Alexander Bortnikov, Russian Foreign Minister Sergei Lavrov, and former head of Russia’s Foreign Intelligence Service Mikhail Fradkov. Photo credit: Kremlin.

All told, it is unclear that sanctions against Russia have achieved any substantive US or EU foreign policy goals. Apart from slowing the pace of military modernization, economic punishment inflicted by the United States and EU has yet to redirect the Kremlin’s strategic calculus or alter Russia’s political and economic ambitions in the Ukraine and the Arctic.

This review of economic sanctions against Russia reveals several valuable insights. First, the absence of a benchmark on the economic losses needed to change Russian policy severely limits meaningful assessments of the effectiveness of the current set of sanctions. Second, analyses of the impact of sanctions on Russia fall short on several fronts: volatile global economic events blur the sanctions’ effects and thereby their “powers of persuasion”; data limitations at the country, sector, and firm levels are severe, hobbling accurate quantification of sanctions’ impacts; and anecdotes and “guesstimates” inform the discourse on sanctions’ effectiveness, but are left unchallenged by rigorous analysis. This detailed investigation into the alignment of the US-EU sanctions on Russia over the annexation of Crimea demonstrates the challenges of aligning economic sanctions. Inabilities to overcome these challenges suggest these sanctions, at this juncture, should be considered poorly aligned.20

Conclusion

Aligning economic sanctions is a difficult goal to achieve, but the credibility of economic sanctions as a vital foreign policy tool depends upon it. The existing body of research on economic sanctions and their effectiveness—and the more general discussion about the challenges of aligning economic sanctions and detailed assessment of US and EU economic sanctions on Russia provided in this brief—all confirm the ineffectiveness of poorly aligned economic sanctions.

Moving forward, efforts to better align economic sanctions would benefit from several initiatives, including the following:

Developing analytic techniques that estimate the level of economic costs needed to change the policies of other governments, the portion of those economic costs achievable through economic sanctions, and the cost of economic sanctions on others in the sanctioned and sanctioning countries. • Establishing robust and continually updated databases and analytics for risk and scenario analyses to inform the design of economic sanctions that have high probabilities of achieving specified economic impacts.

Anticipating that economic sanctions will need to be flexible and adjusted on a regular basis to stay aligned in response to changing global market conditions and evasive actions by the sanctioned country.

Avoiding using economic sanctions as symbolic foreign policy gestures.

Encouraging greater reliance on multilateral economic sanctions by creating a forum where countries can share data and other information about the potential and actual impact of alternative economic sanctions regimes.

No comments:

Post a Comment