Domestic production looks set to peak, with some profound implications for the world market.

Intense focus on the North American shale boom, Saudi Arabia, and ISIS obscures an important emerging energy trend: China’s oil production is peaking. This has profound implications for the world oil market, because China is not just a massive importer of crude; it is also among the world’s five largest oil producers, trailing only the U.S., Russia, and Saudi Arabia, and virtually neck-in-neck with Canada.

Intense focus on the North American shale boom, Saudi Arabia, and ISIS obscures an important emerging energy trend: China’s oil production is peaking. This has profound implications for the world oil market, because China is not just a massive importer of crude; it is also among the world’s five largest oil producers, trailing only the U.S., Russia, and Saudi Arabia, and virtually neck-in-neck with Canada.

China’s oil industry has delivered impressive oil and gas production growth over the past decade. Yet a range of data and historical analogies increasingly suggest that, at global oil prices between $50-to-$100 per barrel, China’s oil supply capability is plateauing and may peak as soon as this year. Lower or higher prices would accelerate or extend this timing.

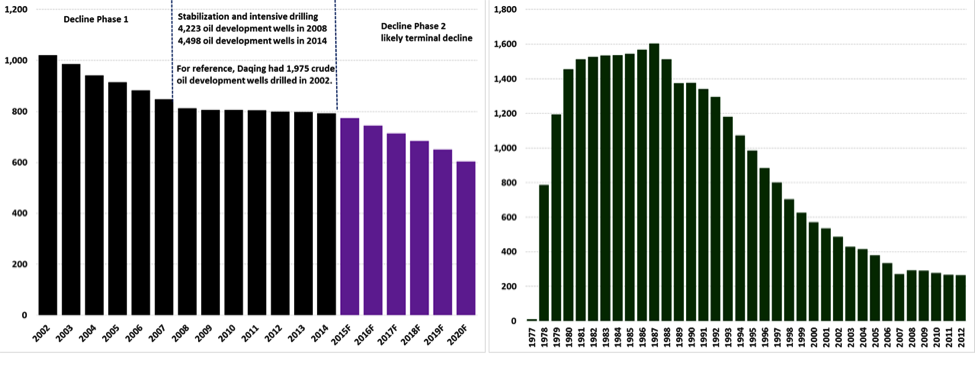

China’s crude oil output has stagnated for the past two years despite intense drilling activity on land and offshore. In late 2014, CNPC essentially threw in the towel on its workhorse field, Daqing, announcing that it would allow the field to essentially enter a phase of managed decline over the next five years. Under this new approach, the field’s oil production will fall from 800,000 barrels per day (kbd) in 2014 to 640 kbd by 2020: a 20 percent decrease. To highlight the importance of PetroChina’s decision, consider that Daqing currently accounts for approximately one in every five barrels of oil currently pumped in China – on par with the role Alaska’s massive Prudhoe Bay field has played in U.S. oil production.

While Daqing’s output has thus far declined less steeply than Prudhoe Bay’s, the Prudhoe experience shows that for even a massive field, once the steep stage of the terminal decline output phase begins, there is generally no turning back (Exhibit 1).

Exhibit 1: Oil Production Trajectories of Daqing and Prudhoe Bay, ‘000 bpd

Daqing Prudhoe Bay

Source: Alaska Oil & Gas Conservation Commission, PetroChina, EIA, Author’s Analysis

Daqing’s oil production has declined relentlessly, despite PetroChina’s significant increase in drilling activity in the field during recent years. This suggests a significant risk that production could fall faster than planned. For reference, PetroChina drilled 1,975 development wells in 2002 when oil production averaged 1.079 million barrels per day, but was forced to boost this to 4,498 development wells in 2014, when oil output at Daqing averaged 792,000 barrels per day. In short, the number of development wells drilled increased by nearly 250 percent while oil production fell by roughly 27 percent.

Unconventional Production

The oil industry consistently deploys ingenuity and technology to break through many geological and economic barriers. China has large potential shale oil reserves, as many as 32 billion barrels of which are technically recoverable, according to the EIA. However, aboveground barriers created by politics and local legal, regulatory, and ownership systems constrain development.

Combine such hurdles and disincentives to innovation with complicated shale geology, and the outlook for commercial-scale development in the next five to seven years becomes dim. The fundamental question is this: Can China bring unconventional oil online in time, and in sufficient measure, to offset terminal oil output declines in its workhorse conventional oilfields?

The short answer increasingly appears to be “no.” Four key factors restrain Chinese crude oil output, which will most likely remain at or below the 4.25 million barrel per day mark. The first factor is a global one: low crude oil prices. The breakeven costs of Chinese oilfields vary and data on this important metric are scarce. But what is clear is that China’s core oilfields – especially Daqing and Shengli – are older, suffer from significant reservoir depletion, and require intensive enhanced recovery techniques that eat into profitability. In an uncertain oil price environment, this reduces producers’ incentives to boost drilling to the point necessary to potentially increase production.

The second factor is more specific to China: declining old geology and complex new geology. Even if PetroChina and Sinopec did significantly increase their drilling activity at Daqing and Shengli, production returns would likely be marginal at best. As cited above, Daqing production drilling rose by a factor of nearly 2.5 between 2002 and 2014, yet oil output fell by more than 25 percent.

Factor three is China’s unconventional oil production potential. With the old fields declining, one may ask: Can hydraulic fracturing deliver a Chinese shale boom like what the U.S. has experienced? The long answer is that “it’s complicated” but the short answer is generally “no.” China’s unconventional oil deposits are more challenging to work with than North American ones. North American tight and shale oil plays tend to have been deposited by ancient seas, while China’s hydrocarbon-bearing shales were left behind by prehistoric lakes, leaving rock layers that are more ductile and less “fracable” than brittle marine shales.

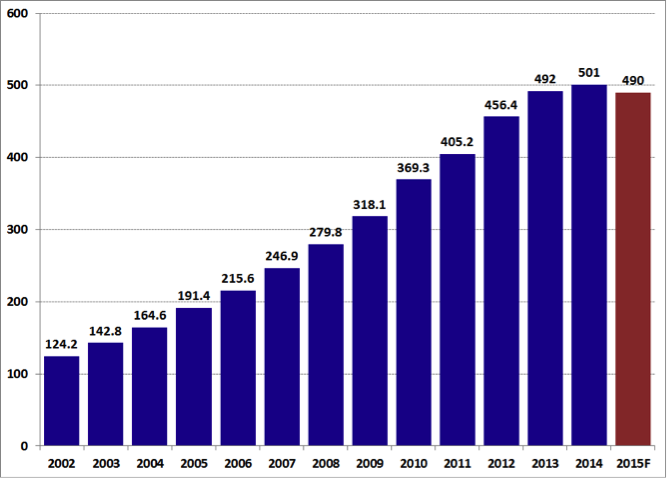

There are some areas with promising tight oil potential. For instance, the Changqing Field in the Ordos Basin of Northwest China – China’s signature tight oil play to date – has seen production grow from 124 kbd in 2002 to 500 kbd in 2014 (Exhibit 2). However, Changqing’s production growth rate has slowed significantly over the past three years and appears poised to decline slightly in 2015, based on first quarter production of 487 kbd, which was lower than the 2014 average production figure despite a relatively mild winter. The drop suggests that low prices slowed drilling activity in the Ordos Basin, although this author has not yet seen explicit confirmation of this.

Exhibit 2: Slowing Changqing Output Suggests Tight Oil Insufficient to Offset Core Fields’ Decline

Source: PetroChina, Author’s Analysis

Despite some recent announcements of additional tight oil discoveries, Changqing’s slowing production growth rate over the past three or four years contrasts sharply with the hyperbolic production growth seen during the booms in world-class tight oil plays like the Bakken and Eagle Ford shales in the U.S. This difference is critically important because to offset production declines and propel significant net growth in a mature oil province like China or the U.S. requires multiple massively robust unconventional fields.

Yet Chinese tight oil plays so far have not reached nearly such a scale. Data from CNPC show that wells from the Zhuang-183 drilling program had an average test production rate of approximately 750 bpd. That is clearly commercial, but top U.S. shale wells in the Eagle Ford and Bakken can yield initial production (“IP”) rates exceeding 4,000 bpd of oil and liquids. Horizontal wells in the highly productive Permian Basin of Texas and Eastern New Mexico often yield 30-day IP rates of 500 bpd of oil, which will typically translate into an initial production test rate in the same range as CNPC’s Zhuang-183 Ordos horizontal wells.

Above-Ground Factors

To boost production on a national level, China’s oil companies will need to employ industrial-scale drilling that brings thousands of horizontal oil wells online each year. This would entail a quantum leap from the 1,610 horizontal wells CPC drilled in China during 2014, particularly because a significant number of these wellsaimed to find gas. If they attempt this, Chinese producers will likely crash into systemic barriers that in many ways matter far more for unconventional oil and gas development than oil prices or geology do; namely, factors that promote oil and gas sector innovation. Innovation confers an incredible ability to adapt to volatile commodity markets and challenging geological issues.

Herein lies factor four: aboveground limitations on China’s unconventional oil potential. The U.S. shale boom arose in a very unique setting. This analysis certainly is not about U.S. “energy exceptionalism,” but the unique combination of dozens of operators with stock market capitalizations exceeding one billion dollars who enjoy access to deep capital markets, incentives to take risks, and a land and mineral ownership system that provides strong financial motivations for oil and gas development are major pluses that China largely lacks.

Chinese companies are well-positioned to rapidly fill in gaps in the country’s physical oil and gas infrastructure. However, the institutional and legal structures and corporate ecosystem (especially independent drillers) that have driven U.S. unconventional energy development are much harder to replicate. For a case in point, consider how independent U.S. energy producers have driven the fracking boom while the international majors have largely failed to generate organic unconventional oil and gas growth.

Many independent firms such as EOG Resources grow organically by discovering and developing new shale and tight oil plays. Yet the international behemoths like ExxonMobil and Statoil have had to buy their way into unconventional plays after the fact, often finding less success and lower than expected returns when they do. At this point, no evidence suggests CNPC/PetroChina or Sinopec will fare any better at unconventional oil development than the U.S. and European oil majors have.

Offshore Production

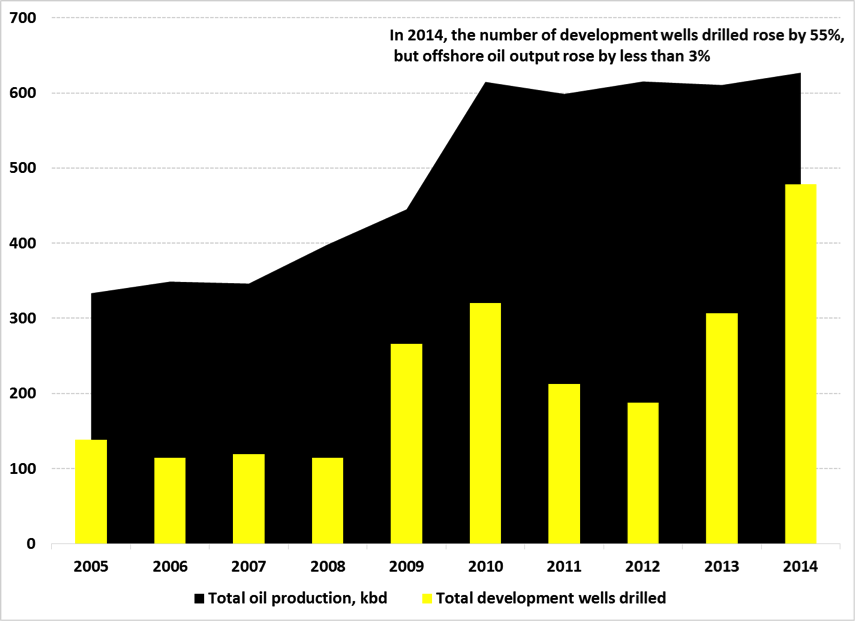

China oil production optimists may point to a handful of offshore projects CNOOC will bring online this year in the Bohai Gulf as evidence that China still has room to expand domestic oil output. For those holding this view, here is the way to put output from new fields in perspective: in 2015, CNOOC plans to activate fields off China that at their peak (likely to come in 2016 or beyond) could produce 108 kbd of oil.

In contrast, assuming a 4 percent natural decline rate in all Chinese oilfields (a conservative assumption), drillers still must bring on nearly 170 kbd of new oil production each year just to compensate for natural depletion and keep production at its current level. CNOOC, which dominates oil production offshore China, forecasts that production of all hydrocarbons will grow very slightly in 2016 and 2017. Because most of China’s large offshore energy discoveries in recent years have been of natural gas field, CNOOC’s reluctance to break down its forecast into oil and gas subdivisions reinforces the growing wave of data suggesting that offshore oil production will not turn the tide of China peak oil (Exhibit 3).

Exhibit 3: Offshore Oil Production Will Not Turn the Tide of Oil Production Declines

Source: CNOOC, Author’s Analysis

Strategic Implications

The latest IEA data estimate that China’s crude oil output in 2015 will average 4.3 million barrels per day. This is likely to be the high-water mark for China’s domestic oil production, as oil price uncertainty and disruption from anti-corruption investigations trim oil executives’ risk appetites in 2015. CNPC and CNOOC, in particular, are very upstream focused and will not drill as aggressively with investigators sniffing around while oil trades at a bit more than half the price it fetched a year ago. But such tactically driven activity declines should not obscure the underlying strategic story: China would still very likely be at peak oil production this year even if oil prices were closer to $100 per barrel.

Looking out to 2020, tight oil output may well increase if drillers can “crack the code” of China’s ductile lacustrine shales. But this oil would simply slow the stasis and impending decline in national crude oil output. The Chinese oil patch does not appear to have any world-class unconventional oil plays like the Bakken, Eagle Ford, or Vaca Muerta poised to emerge within the next five years in a way that would reverse the emerging peak production situation.

It is increasingly likely that if new unconventional oil resources become commercially productive in China, by that time their output will simply compensate for depletion of existing conventional oil resources, rather than actually boosting net oil output as has been the case in the U.S. As things stand, the evidence increasingly points to a future where China’s national oil companies will preside over a gradual crude oil production decline that begins now, in 2015.

Gabe Collins is the co-founder of China SignPost and a former commodity investment analyst and research fellow in the U.S. Naval War College’s Maritime Studies Institute.

No comments:

Post a Comment